We set out the case for global listed property in Mispriced in plain site: The case for global REITs (Part 1). Among global real estate investment trusts (GREITs), valuations are growing, earnings are improving and, across most commercial property sectors, supply is constrained.

For investors keen to take advantage of these dynamics, who appreciate the defensive qualities of particular property types and the prospect of relatively attractive risk-adjusted returns, there is a more urgent question: how best to access the opportunity?

It would be opportune to at this point raise a vested interest. As an active GREIT funds manager, we would naturally make the case for active management. Nevertheless, the facts speak for themselves, this is an active manager’s market. In this article we’ll explain why the Dexus Global REIT Fund portfolio is well placed to take advantage of it.

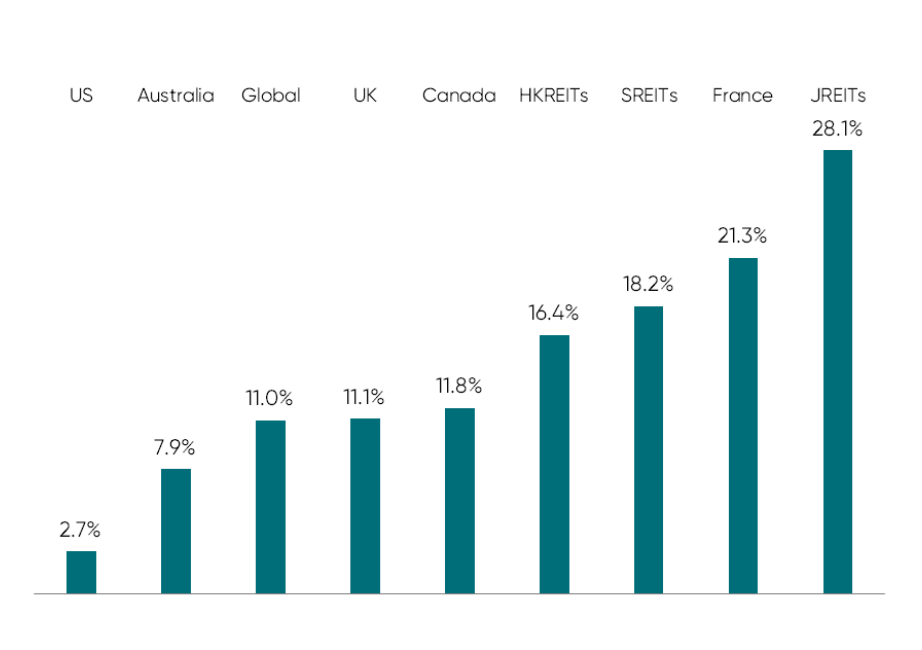

1. Dispersion creates opportunity

In 2025, performance dispersion, the spread of investment returns from their average across global REITs was unusually wide.

Country returns ranged from low single digits to more than 25%. Sub-sector outcomes spanned from negative mid-single digits (residential) to almost 30% (healthcare).

Country Performance CY2025

Source: DXAM, UBS

This is not typical of a market moving in lockstep on macro factors. Instead, it reveals significant differences in Global REIT portfolios and their respective balance sheet strength and management quality. Index returns hide a good part of this story. The average is rarely the most attractive part of the market.

These are not circumstances in which index funds do well because selection is critical to performance. Active managers are forward looking; index funds are built on a view of the past. In performance terms, that contrast is usually most evident when the cycle turns. We believe we have reached such a point.

2. The limits of Index investing

It is a mathematical inevitability that global REIT indices are biased towards large-capitalisation stocks. The chart below makes this case. About 72% per cent of the benchmark’s weighted average is in companies with market capitalisations of over A$9.5 billion.

Weighted average market cap (AUD)

.png)

Source: FactSet, DXAM

These are the most researched and widely owned securities in the sector. They also tend to be held across multiple passive vehicles and large institutional mandates. While this concentration can dampen mispricing, it can work the other way, too. Balance sheet weaknesses or structural challenges can be embedded in index exposures at precisely the wrong point in the cycle.

As the chart shows, the Dexus Global REIT Fund has significantly higher exposure to small and mid-capitalisation stocks that are under-represented in indices and under-covered by research houses. This is where valuation anomalies are more likely to arise. Indeed, this is where we are finding the best opportunities.

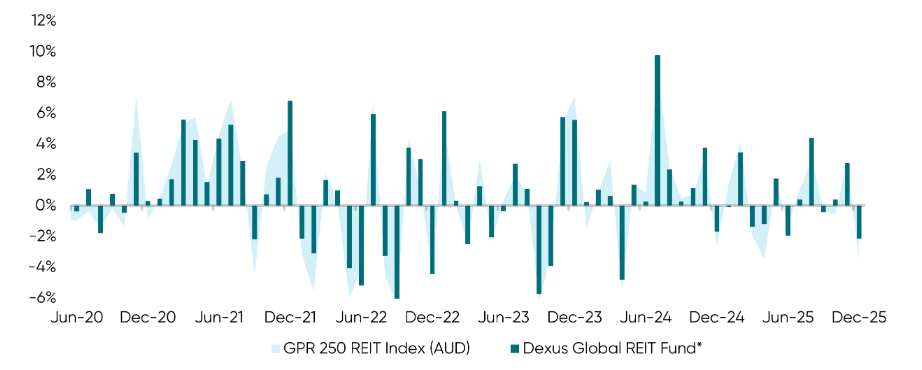

3. Capital preservation focus boosts total returns

The Fund’s objective explicitly emphasises lower volatility, steady income and capital preservation alongside total returns. Capital growth is an important but secondary consideration.

The latter, however, works in concert with the former. In 74% of down markets since inception, the Fund has outperformed the benchmark. This isn’t relevant just to income-focused and risk-averse investors. Avoiding permanent capital impairment during weaker periods compounds over time. It boosts performance.

Periodic Fund vs GPR 250 REIT Net Index*

Source: DXAM as at 31 December 2025

Source: DXAM as at 31 December 2025

Past performance is not a reliable indicator of future performance. Returns after all fees and expenses. Assumes distributions are reinvested. Investors’ tax rates are not taken into account when calculating returns. Returns and values may rise and fall from the one period to another. Fund’s inception date used to determine the return: 1 April 2020. Dexus Global REIT Fund performance Index/Benchmark is the FPR 250 REIT Index (AU).

To 31 December 2025, the Dexus Global REIT Fund has delivered an 8.66% annualised total return since inception on 1 April 2020. This compares favourably to the GPR 250 REIT Net Index (AU) with a comparable total return of 6.93%. These figures, achieved with a focus on capital preservation, are a product of the flexibility that active investing allows. Our current positioning, for example, reflects a willingness to be underweight in areas where expectations appear elevated and overweight in segments where supply constraints and demographic trends are working in our favour. This allows us to target low teens total returns over the coming years whilst maintaining our mandated concentration on capital preservation.

4. Direct markets are validating value

One of the strongest pieces of evidence that our portfolio positioning and composition can deliver on these targets comes beyond the public market.

Direct commercial real estate transaction volumes are improving along with private capital fundraising and debt issuance, as we noted in part 1. But, as the table below shows, there has also been a steady stream of value affirming, take-private transactions and corporate activity in listed property.

| REIT Name | Date | Status | Fund Weight | Index Weight | Total Return |

|---|---|---|---|---|---|

| Bluerock Residential | Dec-21 | Privatisation | 4.00% | 0.00% | 102.89% |

| RPT Realty | Aug-23 | M&A | 4.00% | 0.00% | 22.96% |

| AIR Communities | Apr-24 | Privatisation | 1.20% | 0.40% | 12.81% |

| Retail Opportunity Investments Corp | Nov-24 | Privatisation | 3.00% | 0.14% | 28.73% |

| Urban Logistics REIT Plc. | May-25 | M&A | 3.75% | 0.00% | 48.69% |

| City Office REIT | Jul-25 | Privatisation | 4.00% | 0.00% | 78.72% |

| Plymouth REIT | Oct-25 | Privatisation | 2.00% | 0.00% | 138.20% |

| Kennedy-Wilson Holdings | Nov-25 | Privatisation | 0.75% | 0.00% | 88.34% |

| Alexander & Baldwin | Dec-25 | Privatisation | 1.00% | 0.00% | 42.76% |

Source: FactSet, DXAM

These aren’t theoretical valuation exercises. Private buyers, with long-term capital and detailed asset knowledge, are willing to pay more than the value public markets have ascribed to these assets.

Index funds capture such outcomes only in proportion to their index weights. As an active manager with a 75% active share at the stock level, we capture them more fully and are positioned to do so.

5. Historic discount offers a great opportunity

Global REITs have underperformed global equities for four consecutive calendar years, a record stretch over more than three decades of data. Relative to equities, the sector now trades significantly below historical averages.

In this environment, passive index funds ensure investors own the market’s aggregate exposure, warts and all. Active management helps us concentrate investor capital on companies with defensible cash flows, prudent leverage and exposure to sectors with constrained supply. It also allows us to purchase those GREITs offering the biggest valuation discounts.

The return profile

The best opportunities in global listed property often don’t exist or aren’t material among index ETFs. Dispersion across countries, sectors and individual securities is high. Direct market transactions are validating private values above listed prices while balance sheet strength and asset quality differ markedly.

For investors seeking increased property exposure, with an emphasis on income and capital preservation, this is not a time to own the average. It is a time to be selective.

This is an environment tailor-made for the Dexus Global REIT Fund. The combination of income, valuation support and improving fundamentals among a defensively constructed portfolio of under-researched stocks bolsters our expectation for annual total returns in the mid-teens.

In the next and final part of this series, we’ll examine a few stocks that demonstrate our approach and indicate where we hope to secure such returns.

Invest in GREIT

The Dexus Global REIT Fund (DXGRF) is an investment strategy for global listed property developed to target higher income with low relative risk while maintaining the real value of capital over the investment time horizon. The fund invests in the developed markets of North America, Europe and Asia.

More insights

David Kruth appears on Investment Matters

David Kruth and Darren Connolly explore the evolution of global REIT markets, examining the shift toward modern, growth‑oriented property sectors and the implications for today’s investors.

15 Apr 2026

Webinar: Global REITs – Mispriced in Plain Site

John Taylor and David Kruth sit down to discuss the current mispricing across global listed real estate, highlighting compelling opportunities in Real Estate Investment Trusts (REITs) created by discounts to private market valuations.

11 Mar 2026

Mispriced in Plain Site: The case for Global REITs - Part 3

Part 3 of “Mispriced in Plain Site" shows how the Dexus GREIT Fund turns mispricing into opportunity, backing sectors with structural tailwinds and using active conviction to capture value the index never sees.

03 Mar 2026

Mispriced in Plain Site: The case for Global REITs - Part 1

Global REITs are shaping up as one of the most overlooked opportunities in global markets today. After years of being priced for caution, fundamentals are now strengthening while valuations remain at levels not seen in decades.

25 Feb 2026

8 Lessons from London: What Investors Are Missing in Global REITs

At the recent UBS Global Real Estate Conference in London, a key investing lesson was subtly but forcefully reiterated: stocks can stay mispriced for longer than you might expect.

12 Jan 2026

Global REITs: A mispricing opportunity investors can’t ignore

Global Real Estate Investment Trusts (REITs) are almost always sold on the same two hooks. The first is international diversification—the very sensible idea that you shouldn't have all your eggs in an Australian basket.

02 Dec 2025

DXGRF Q3 2025 Quarterly Snapshot

The Dexus Global REIT Fund achieved a 4.40% return, outperforming its benchmark by 59 basis points. Mark Mazzarella discusses strong stock selection and the Fund's focus on resilient income streams and long-term opportunities, even amid market uncertainty.

14 Nov 2025

The psychology of active REIT investing - Part 2

Active REIT investing requires skill, value focus, patience, and learning from past mistakes to avoid fear of missing out (FOMO)-driven decisions.

08 Oct 2025

Important

This (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”), the responsible entity and issuer of the financial products of Dexus Global REIT mentioned in this Material. DXAM is a wholly owned subsidiary of Dexus (ASX: DXS).

Information in this Material is current as at February 2026 (unless otherwise indicated), is for general information purposes only, does not constitute financial product advice and does not purport to contain all information necessary for making an investment decision. It is provided on the basis that the recipient will be responsible for assessing their own financial situation, investment objectives and particular needs. Before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), investors should read the relevant product disclosure statement (“PDS”), financial services guide (“FSG”) and target market determination (“TMD”) in full, and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1800 996 456. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material does not constitute an offer, invitation, solicitation or recommendation to subscribe for, purchase or sell any financial product, and does not form the basis of any contract or commitment. This Material must not be reproduced or used by any person without DXAM’s prior written consent. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives.

Any forward-looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward-looking statements for a range of reasons. Past performance is not an indication of future performance. The forward-looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments.

Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material. By reading or viewing this Material and to the fullest extent permitted by law, the recipient releases Dexus, DXAM, their affiliates, and all of their directors, officers, employees, representatives and advisers from any and all direct, indirect and consequential losses, damages, costs, expenses and liabilities of any kind (“Losses”) arising in connection with any recipient or person acting on or relying on anything contained in or omitted from this Material or any other written or oral information, statement, estimate or opinion, whether or not the Losses arise in connection with any negligence or default of Dexus, DXAM or their affiliates, or otherwise.

Dexus, DXAM and/or their affiliates may have an interest in the financial products, and may earn fees as a result of transactions, mentioned in this Material.

How can we help?

Connect with us to explore investment opportunities, find the right space for your best work or learn more about what we do. Together, let’s create tomorrow.