Global Real Estate Investment Trusts (REITs) are almost always sold on the same two hooks. The first is international diversification—the very sensible idea that you shouldn't have all your eggs in an Australian basket.

The second is access to property sectors that simply don’t exist on the ASX, including seniors living, for-rent residential and vast data centre networks.

These arguments, whilst true, are straight from the brochure. As active managers, this is not our pitch. We don't buy stocks to satisfy a sector pie-chart. We buy access to durable growing cash flows, capable management teams, strong balance sheets and aim to do so at a reasonable price. And right now, the signal flashing from the global real estate market is one of the most compelling in years.

In our view, there is a profound disconnect between the price you pay for listed real estate and the value of the assets an investor ultimately owns. If you’re seeking to protect your portfolio with real assets but still enjoy growing, stable yields with capital growth potential, this disconnect delivers a rare opportunity.

Before dissecting it, let me explain our view of the world. The Dexus investment philosophy is anchored in the belief that, above all, commercial property is an investment in a predictable, growing income stream.

Unlike equities, where earnings can quickly evaporate through changes in consumer preferences or technological disruption, high-quality real estate is bound by long-term leases as well as high barriers to entry. These qualities offer sturdy protection from the short-term business cycle that often impacts other asset classes with the benefits magnified by active management.

But not all REITs are created equal, which is why we aren’t interested in buying an index. Instead, while we manage a portfolio diversified by geography and asset type, our focus is on owning global REITs benefiting from sustained rental tension, which in real estate terms means rental pricing power. This ultimately drives total return and investment performance, in our view.

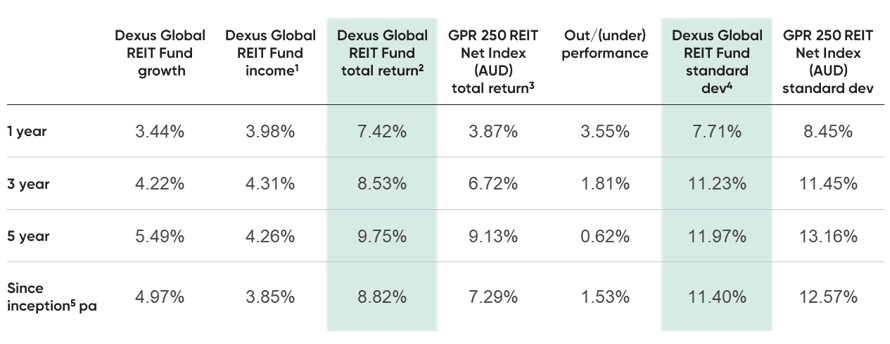

This focus has helped the Fund deliver superior relative total returns, income and lower volatility:

1. Distributions may include a capital gains component.

2. Returns after all fees and expenses to 31 October 2025. Assumes distributions are reinvested. Investors’ tax rates are not taken into account when calculating returns. Returns and values may rise and fall from one period to another. Fund’s inception date used to determine the return: 1 April 2020. Current running yield is calculated daily by dividing the annualised distribution rate by the latest entry unit price. Distributions may include a capital gains component. Distributions are not guaranteed. On 31 October 2025, the Fund changed its performance benchmark from GPR 250 REIT Index (AU), where returns are calculated on a “gross” basis with respect to withholding taxes, to GPR 250 REIT Net Index (AU), which is on a “net” basis. The new benchmark allows for a more accurate comparison of benchmark and Fund returns. The impact of the change on the comparison of Fund’s performance returns to the benchmark is not material and accordingly, the Fund’s inception date used for since inception returns remains 1 April 2020.

3. Dexus Global REIT Fund performance Index/Benchmark is the GPR 250 REIT Net Index (AU)

4. Calculated monthly, Standard deviation is based on total returns (net of all fees).

5. Fund inception 1 April 2020.

*Portfolio statistics sourced from Bloomberg and calculated since Fund inception 1 April 2020

Thanks to the current rental tension, the prospects for sustained rental growth and total return are set to continue. Let me explain why.

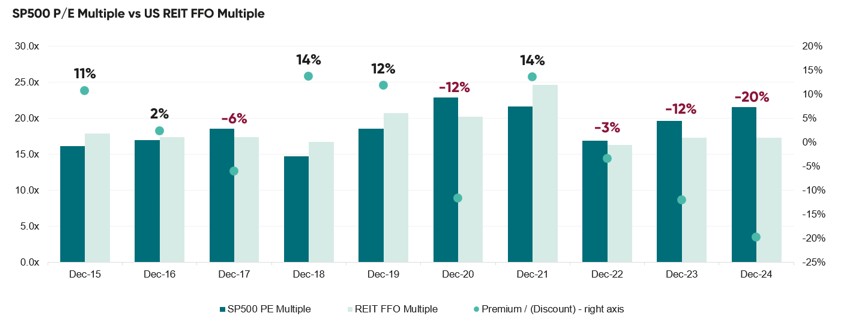

For the last few years, global real estate earnings have been fighting a headwind. That is beginning to change but current prices do not reflect this fact. As the chart below shows, GREIT multiples are trading at their widest multiple gap to equities in 10 years.

Relative value on offer in Global REITS

REIT multiples are trading at the widest mukltiple gap to equities in 10 years.

Jefferies Research, DXAM, as at June 2025

Meanwhile, operational fundamentals are strengthening. While global GDP growth is forecast to remain sluggish—hovering around 1.4% to 1.7%—global real estate earnings per share growth (EPS) is forecast to accelerate sharply, hitting 6.5% in 2025.

UBS Research

Historical gloval real estate sectore earnings growth vs. GDP growth*

Source: IBES, Datastream, UBS, DXAM

*This graph has not been prepared by DXAM and the information in it is predictive in nature. Global EPS & GDP growth (YoY) is average of US, UK, EU, AU, JP, HK, and Singapore. Any forward looking statements are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. The statements may therefore be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Actual results ultimately achieved may differ materially from those predicted or implied by any forward looking statements and are not guaranteed to occur. The forward looking statements only speak as at the date of this material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments. Past performance is not a reliable indicator of future performance.

When real estate earnings growth outpaces the broader economy by such a wide margin, it indicates that landlords have pricing power. Supply constraints in key sectors are allowing rents to rise even as the wider economy cools.

This is reflected in earnings growth which, after a few testing years, has reached an inflection point, a fact that the "smart money" has already noticed but the broader market has not.

In the first half of 2025, global listed real estate transaction volumes hit US$358 billion, up from US$295 billion in the previous corresponding period. Public markets may be pessimistic but those with capital—largely pension funds and private equity—are stepping in to close the gap, buying entire companies at a discount. This is another value-affirming signal.

The macroeconomic backdrop is also favourable. Investors often worry about bond yields acting as a gravitational pull on real estate prices but the “spread” between GREIT EPS yields and local 10-year bond yields remains attractive. In almost every major market the earnings yield on REITs sits comfortably above the risk-free rate.

But we must return to basic financial ratios for the most striking comparison between global REITs and general equities.

Historically, listed real estate and general equities have moved more or less in tandem. The pandemic took a hammer to that relationship. No matter the metric used, GREITs look attractive when compared to general equities.

On a price-to-cash-flow basis, GREITs are trading at levels significantly below their 10-year average while general equities trade at elevated multiples. The same applies to price-to-book value and, as mentioned above, price-to-earnings ratios (PER).

On most measures, GREITs are trading at their widest discount to equities in a decade, and sometimes even longer.

UBS Research, DXAM

For active managers like us, this is the sweet spot. We are being offered assets with superior earnings growth forecasts at valuation multiples that look like they’re distressed when they’re anything but.

So, what does this opportunity look like on the ground? Let me offer two examples from our portfolio: Plymouth REIT in the US and Urban Logistics REIT in the UK.

Plymouth REIT (NYSE: PLYM) is a classic example of an unloved stock where the intrinsic value was hiding in plain sight. Plymouth specialises in "small bay" industrial properties— smaller warehouses and flex spaces that are the lifeblood of the US manufacturing supply chain.

The market had priced Plymouth at an implied capitalisation rate of 9.3%. In plain English, the market was saying these buildings were risky or low quality. In contrast, we found a portfolio of 204 industrial buildings concentrated in key manufacturing regions, generating steady cash flow.

Our thesis was validated when a private Equity (PE) firm launched an unsolicited, non-binding bid for the company at an implied a cap rate of 7.5%—a substantial repricing from the market’s 9.3% assessment. This outcome resulted in a year-to-date total return in excess of 30% and was a textbook example of the private market stepping in to close the discount to fair value, benefiting our investors.

In the UK, Urban Logistics REIT (LSE: SHED) was a similar example. This REIT comprised a curated portfolio of "last mile" warehouses essential for getting goods to customers' doors in crowded urban cities.

Despite high-quality fundamentals and a portfolio ripe for organic growth through rent increases, the stock has been trading at a significant discount. However, investors agitated for the company to close the discount to fair value and ultimately succeeded. The rental growth was real, the assets essential but the market’s assessment of value anomalous, resulting in a much larger listed peer taking it over for a handsome premium.

These are not isolated examples of market inefficiency. Global REITs currently offer a "free lunch" of sorts, offering higher yields and higher growth at lower multiples than the broader market.

But capturing opportunities like this requires more than simply buying an index fund. The difference in performance between the best and worst assets is widening. The environment calls for an active manager to identify the specific sub-sectors where supply is tight and the specific companies where the discount to private market value is too large to ignore.

That’s what the Dexus GREIT Fund is all about. For investors seeking protection in an uncertain world, the combination of a reliable, growing yield and the potential for significant capital appreciation as these valuation gaps close is a compelling proposition. International diversification is a bonus; the real prize is the value on offer.

Invest in GREITs

Focusing on sustainable growth, regular returns and lower-than-market volatility, the Dexus Global REIT Fund (DXGRF) is an actively managed property securities fund investing in a diversified portfolio of Real Estate Investment Trusts listed in North America, Europe and Asia Pacific.

More insights

David Kruth appears on Investment Matters

David Kruth and Darren Connolly explore the evolution of global REIT markets, examining the shift toward modern, growth‑oriented property sectors and the implications for today’s investors.

15 Apr 2026

Webinar: Global REITs – Mispriced in Plain Site

John Taylor and David Kruth sit down to discuss the current mispricing across global listed real estate, highlighting compelling opportunities in Real Estate Investment Trusts (REITs) created by discounts to private market valuations.

11 Mar 2026

Mispriced in Plain Site: The case for Global REITs - Part 3

Part 3 of “Mispriced in Plain Site" shows how the Dexus GREIT Fund turns mispricing into opportunity, backing sectors with structural tailwinds and using active conviction to capture value the index never sees.

03 Mar 2026

Mispriced in Plain Site: The case for Global REITs - Part 2

With valuations improving and dispersion creating clear winners and losers, this is not a time to own the average. The Dexus Global REIT Fund targets the most compelling opportunities globally, backed by active stock selection and a focus on capital preservation.

26 Feb 2026

Mispriced in Plain Site: The case for Global REITs - Part 1

Global REITs are shaping up as one of the most overlooked opportunities in global markets today. After years of being priced for caution, fundamentals are now strengthening while valuations remain at levels not seen in decades.

25 Feb 2026

8 Lessons from London: What Investors Are Missing in Global REITs

At the recent UBS Global Real Estate Conference in London, a key investing lesson was subtly but forcefully reiterated: stocks can stay mispriced for longer than you might expect.

12 Jan 2026

DXGRF Q3 2025 Quarterly Snapshot

The Dexus Global REIT Fund achieved a 4.40% return, outperforming its benchmark by 59 basis points. Mark Mazzarella discusses strong stock selection and the Fund's focus on resilient income streams and long-term opportunities, even amid market uncertainty.

14 Nov 2025

The psychology of active REIT investing - Part 2

Active REIT investing requires skill, value focus, patience, and learning from past mistakes to avoid fear of missing out (FOMO)-driven decisions.

08 Oct 2025

Important

This (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”), the responsible entity and issuer of the financial products of Dexus Global REIT mentioned in this Material. DXAM is a wholly owned subsidiary of Dexus (ASX: DXS).

Information in this Material is current as at December 2025 (unless otherwise indicated), is for general information purposes only, does not constitute financial product advice and does not purport to contain all information necessary for making an investment decision. It is provided on the basis that the recipient will be responsible for assessing their own financial situation, investment objectives and particular needs. Before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), investors should read the relevant product disclosure statement (“PDS”), financial services guide (“FSG”) and target market determination (“TMD”) in full, and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM, Level 5, 80 Collins Street (South Tower), Melbourne VIC 3000, by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1800 996 456. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material does not constitute an offer, invitation, solicitation or recommendation to subscribe for, purchase or sell any financial product, and does not form the basis of any contract or commitment. This Material must not be reproduced or used by any person without DXAM’s prior written consent. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives.

Any forward-looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward-looking statements for a range of reasons. Past performance is not an indication of future performance. The forward-looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments.

Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material. By reading or viewing this Material and to the fullest extent permitted by law, the recipient releases Dexus, DXAM, their affiliates, and all of their directors, officers, employees, representatives and advisers from any and all direct, indirect and consequential losses, damages, costs, expenses and liabilities of any kind (“Losses”) arising in connection with any recipient or person acting on or relying on anything contained in or omitted from this Material or any other written or oral information, statement, estimate or opinion, whether or not the Losses arise in connection with any negligence or default of Dexus, DXAM or their affiliates, or otherwise.

Dexus, DXAM and/or their affiliates may have an interest in the financial products, and may earn fees as a result of transactions, mentioned in this Material.

How can we help?

Connect with us to explore investment opportunities, find the right space for your best work or learn more about what we do. Together, let’s create tomorrow.