In Mispriced in plain site: The case for global REITs - Part 1, we argued that, despite improving fundamentals, global REITs are trading at rare discounts to global equities.

Part 2 explained how best to take advantage of this opportunity. Dispersion across sectors and regions makes stock selection critical, with the active approach of the Dexus GREIT Fund tailor-made to exploit the gap between price and value.

Here, we’re moving from theory to practice, covering two global REITs that demonstrate our approach in sectors benefiting from structural tailwinds, rental tension and attractive valuations.

Industrial and logistics: The persistence of e-commerce

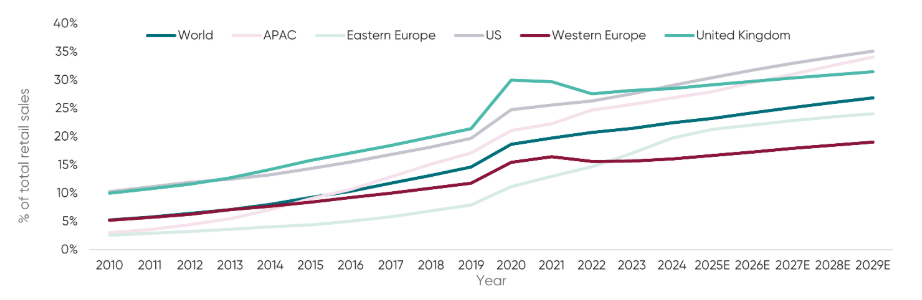

After the dramatic rise during the pandemic, across the world the penetration of ecommerce has continued at pace. This ongoing structural shift in consumption channel is evidenced by the chart below, showing the percentage of total sales taking place online across developed global markets:

Global e-commerce penetration is increasing

Source: Euromonitor International, UBS Research, Jefferies, JLL Research, DXAM

The elevated supply that occurred during Covid has now been almost fully absorbed. In addition, reshoring, driven by the desire to reduce supply chain dependencies, has increased manufacturing demand in North America and Europe.

Supply, meanwhile, has yet to fully respond. The markets are characterised by strict development constraints and long lead times. The barriers work in favour of those REIT portfolios already established. Many are benefiting from what commercial property analysts call ‘rental tension’, where growing demand and restricted supply enjoin to deliver rental increases to existing properties.

In the UK, Urban Logistics REIT (LSE: SHED) was a prime example. This REIT comprised a curated portfolio of ‘last mile’ warehouses essential for getting goods to customers' doors in crowded urban cities.

Despite high-quality fundamentals and a portfolio ripe for organic growth through rent increases, the stock had been trading at a significant discount.

Our thesis rested on four elements. Firstly, a pure-play exposure to the ecommerce trend. Secondly, the company had recently acquired assets that were being rented at below market rates. When those leases expired, we thought it highly likely they would be re-rented at higher rates.

Thirdly, the company’s portfolio was actively managed and well run. There was plenty of potential for earnings to substantially increase. The final point was perhaps the strongest, an implied capitalisation rate materially above private transaction levels.

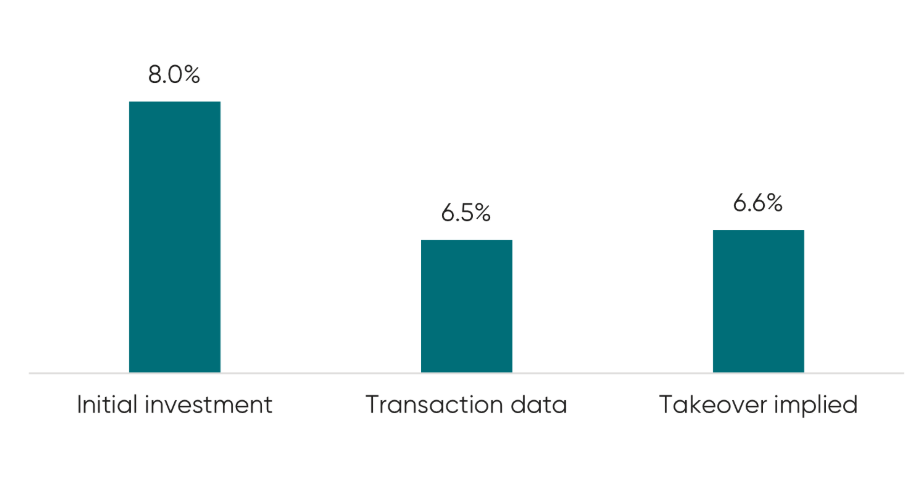

Implied cap rate (%)

Source: DXAM Research

Our initial investment reflected an 8.0% implied cap rate but transaction evidence pointed to a more realistic cap rate of 6.5–6.6%. That 150 basis point spread implied substantial equity mispricing.

That’s how things played out. The potential rental growth eventuated but the market’s assessment of value was anomalous, prompting investors to lobby the company to close the discount to fair value. Ultimately, they were successful. A much larger listed peer took over Urban Logistics for a handsome premium of 33%.

This would have made no difference to the GREIT benchmark fund, which held a weighting of exactly 0% in the stock. In the Dexus GREIT Fund, however, a weighting of 3.75%, meaningfully added to our outperformance.

When public equity markets price assets at discounts to private market values, corporate activity often arbitrages the gap, with merger and acquisition activity often the catalyst.

This is a practical example of how investors can profit from active management in a way that index huggers cannot.

If anything, the supply/demand imbalance in some areas of industrial property are even stronger in the North American REIT sector for real estate portfolios providing for retirement and assisted living.

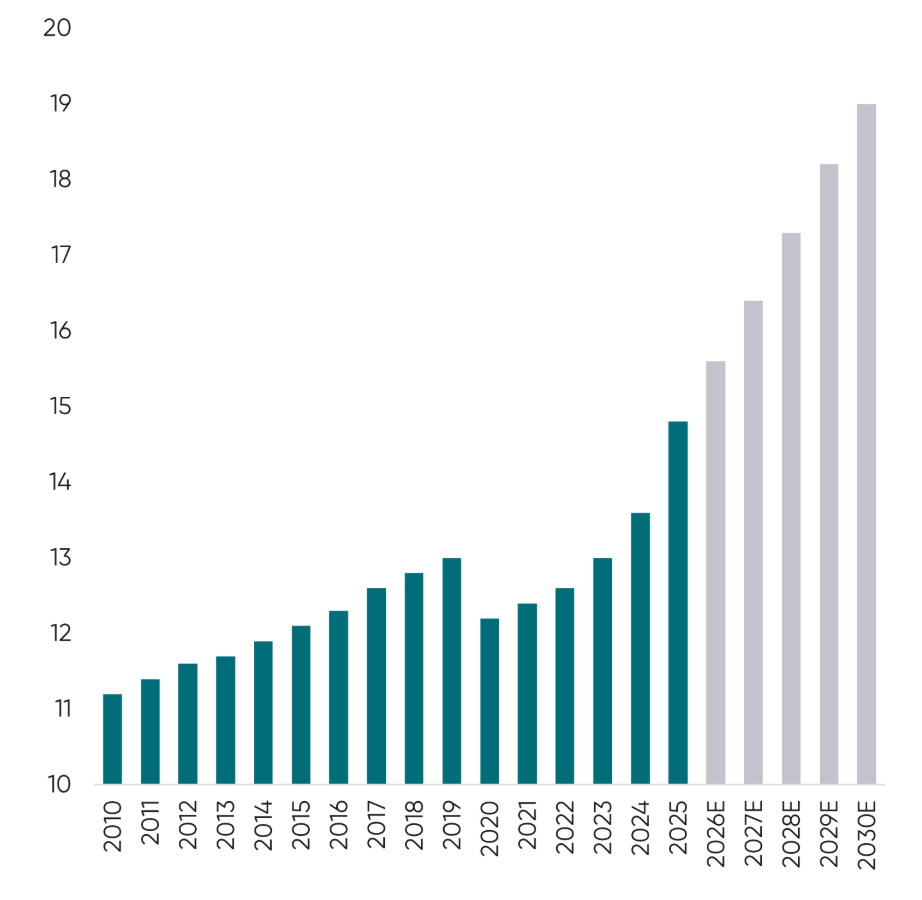

The arithmetic is compelling. Over the last 15 years, the compound annual growth rate of seniors over 80 in the United States has been 1.4%. Between 2026 and 2030, that figure is set to rise to 5%, a more than three-fold increase.

U.S. population aged +80yrs

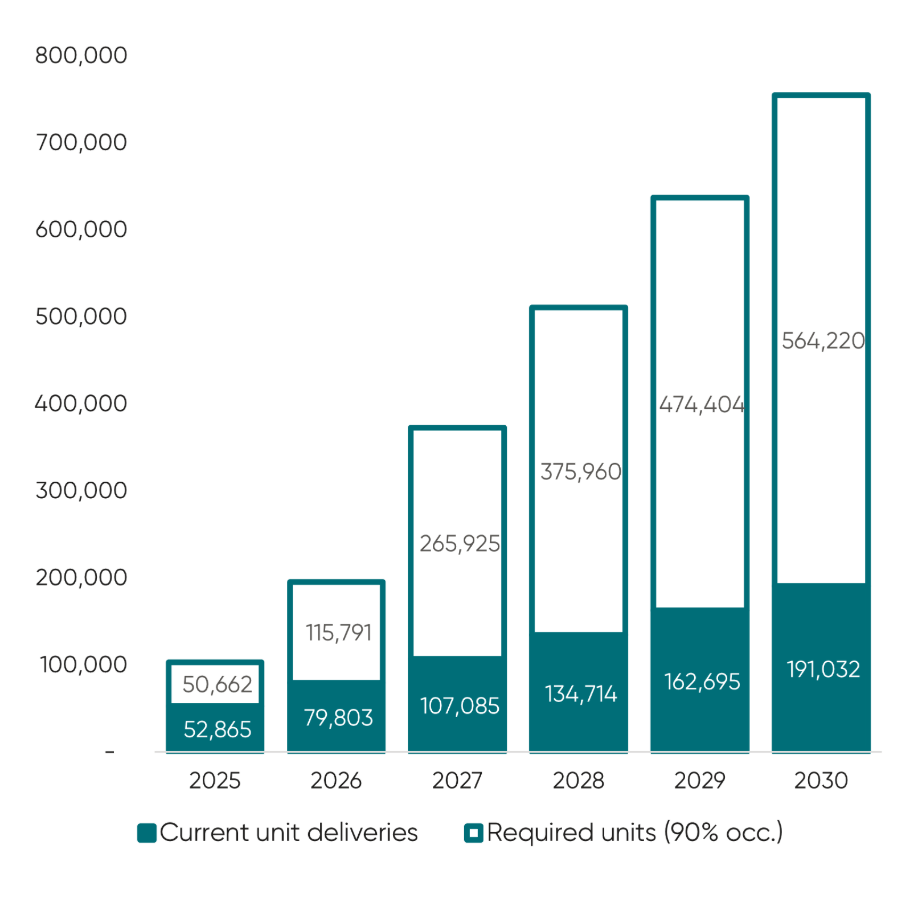

Annual unit development (Current vs. required)

Assuming 90% occupancy

Source1: NIC MAP Vision, Jefferies, OECD, DXAM

Assuming 90% occupancy, required unit delivery far exceeds current construction. The supply gap, already clear in the chart above (right), widens materially through 2030.

For operators, supply constraints will almost certainly lead to improving occupancy and pricing power. As occupancy rises, incremental revenue adds to net operating income because seniors housing has a largely fixed cost base.

The total return potential is clear, which is why assisted living is the Fund’s largest exposure at over 24%. This weighting reflects our conviction in where earnings momentum is clearest and stands in stark contrast to the GREIT index weighting of 12.65%.

Toronto listed Chartwell Retirement (TSE: CSH.UN) is a clear expression of our conviction.

The first pillar in the argument concerns the demographic inevitability of an ageing population. Canada’s 75+ population is expected to double over the next 20 years. Combined with historically low new construction across North America, the supply-demand gap is widening.

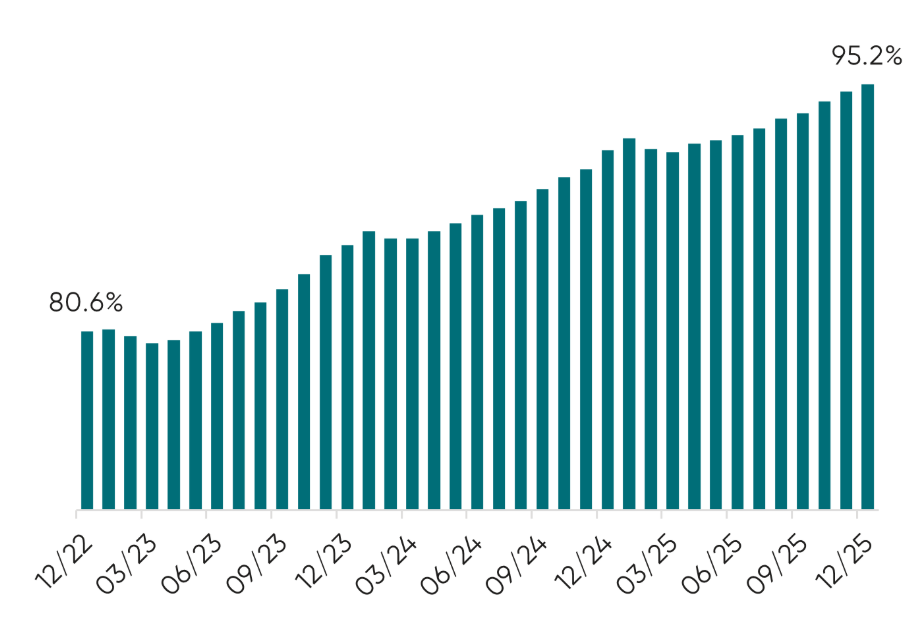

The second is operating leverage. Same-property occupancy has already increased from 80.6% in 2022 to 95.2% in 2025. In a sector with high fixed costs, this 1,450 basis point improvement is a big driver of net operating income.

Chartwell same property occupancy

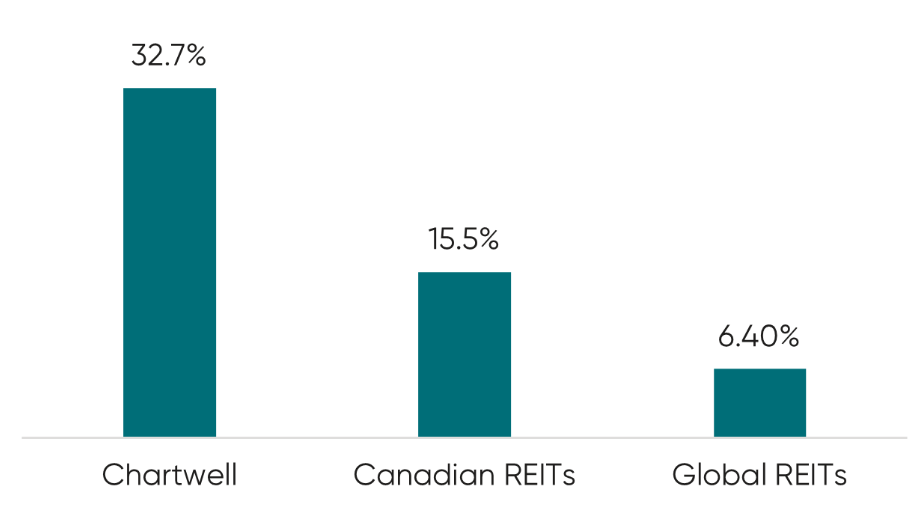

5Y Annualised total return

Source: DXAM Research

We hold a 4.0% position in Chartwell versus a 0% benchmark weight. That active exposure matters and will drive positive outcomes for investors, in our view.

The performance figures reinforce the operating story. Five-year annualised total return was 32.7%, compared with 15.5% for Canadian REITs and 6.4% for Global REITs. That degree of outperformance rarely occurs without both earnings growth and multiple expansion.

Importantly, with occupancy reaching the highest level in company history, the sector may still be in the early innings of its earnings cycle rather than at peak conditions.

For investors, the lesson is not simply that Chartwell performed well. It is that public markets were slow to recognise improving fundamentals. Our active positioning ahead of full recognition generated excess returns.

Both examples underscore why index exposure struggles in this environment and active management excels.

Neither stock had benchmark weight and both delivered alpha through our conviction positioning. And in both cases, the closing of the price–value gap was measurable in occupancy, cap rates and realised returns.

This is what the Dexus GREIT Fund is all about and why we are targeting low teens returns. For investors seeking protection in an uncertain world, the combination of a reliable, growing yield and the potential for significant capital appreciation as valuation gaps close is a compelling proposition.

1. Any forward looking statements are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. The statements may therefore be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Actual results ultimately achieved may differ materially from those predicted or implied by any forward looking statements and are not guaranteed to occur. The forward looking statements only speak as at the date of this material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments.

Invest in GREIT

The Dexus Global REIT Fund (DXGRF) is an investment strategy for global listed property developed to target higher income with low relative risk while maintaining the real value of capital over the investment time horizon. The fund invests in the developed markets of North America, Europe and Asia.

More insights

David Kruth appears on Investment Matters

David Kruth and Darren Connolly explore the evolution of global REIT markets, examining the shift toward modern, growth‑oriented property sectors and the implications for today’s investors.

15 Apr 2026

Webinar: Global REITs – Mispriced in Plain Site

John Taylor and David Kruth sit down to discuss the current mispricing across global listed real estate, highlighting compelling opportunities in Real Estate Investment Trusts (REITs) created by discounts to private market valuations.

11 Mar 2026

Mispriced in Plain Site: The case for Global REITs - Part 2

With valuations improving and dispersion creating clear winners and losers, this is not a time to own the average. The Dexus Global REIT Fund targets the most compelling opportunities globally, backed by active stock selection and a focus on capital preservation.

26 Feb 2026

Mispriced in Plain Site: The case for Global REITs - Part 1

Global REITs are shaping up as one of the most overlooked opportunities in global markets today. After years of being priced for caution, fundamentals are now strengthening while valuations remain at levels not seen in decades.

25 Feb 2026

8 Lessons from London: What Investors Are Missing in Global REITs

At the recent UBS Global Real Estate Conference in London, a key investing lesson was subtly but forcefully reiterated: stocks can stay mispriced for longer than you might expect.

12 Jan 2026

Global REITs: A mispricing opportunity investors can’t ignore

Global Real Estate Investment Trusts (REITs) are almost always sold on the same two hooks. The first is international diversification—the very sensible idea that you shouldn't have all your eggs in an Australian basket.

02 Dec 2025

DXGRF Q3 2025 Quarterly Snapshot

The Dexus Global REIT Fund achieved a 4.40% return, outperforming its benchmark by 59 basis points. Mark Mazzarella discusses strong stock selection and the Fund's focus on resilient income streams and long-term opportunities, even amid market uncertainty.

14 Nov 2025

The psychology of active REIT investing - Part 2

Active REIT investing requires skill, value focus, patience, and learning from past mistakes to avoid fear of missing out (FOMO)-driven decisions.

08 Oct 2025

Important

This (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”), the responsible entity and issuer of the financial products of Dexus Global REIT mentioned in this Material. DXAM is a wholly owned subsidiary of Dexus (ASX: DXS).

Information in this Material is current as at February 2026 (unless otherwise indicated), is for general information purposes only, does not constitute financial product advice and does not purport to contain all information necessary for making an investment decision. It is provided on the basis that the recipient will be responsible for assessing their own financial situation, investment objectives and particular needs. Before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), investors should read the relevant product disclosure statement (“PDS”), financial services guide (“FSG”) and target market determination (“TMD”) in full, and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1800 996 456. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material does not constitute an offer, invitation, solicitation or recommendation to subscribe for, purchase or sell any financial product, and does not form the basis of any contract or commitment. This Material must not be reproduced or used by any person without DXAM’s prior written consent. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives.

Any forward-looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward-looking statements for a range of reasons. Past performance is not an indication of future performance. The forward-looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments.

Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material. By reading or viewing this Material and to the fullest extent permitted by law, the recipient releases Dexus, DXAM, their affiliates, and all of their directors, officers, employees, representatives and advisers from any and all direct, indirect and consequential losses, damages, costs, expenses and liabilities of any kind (“Losses”) arising in connection with any recipient or person acting on or relying on anything contained in or omitted from this Material or any other written or oral information, statement, estimate or opinion, whether or not the Losses arise in connection with any negligence or default of Dexus, DXAM or their affiliates, or otherwise.

Dexus, DXAM and/or their affiliates may have an interest in the financial products, and may earn fees as a result of transactions, mentioned in this Material.

How can we help?

Connect with us to explore investment opportunities, find the right space for your best work or learn more about what we do. Together, let’s create tomorrow.