Tax-deferred income is a powerful and under-rated feature of commercial property investment. For investors seeking reliable, regular income and long-term tax efficiency, understanding how tax-deferred distributions work – and their implications for portfolio strategy – is essential.1

What Is Depreciation?

Buildings don’t last forever – they depreciate over time. There’s no direct cash cost of ‘ageing’ but nevertheless it’s a real cost to investors. In most cases, after around 40 years physical buildings will have exhausted their economic value and therefore each year 2.5% of the original construction cost can be treated as a tax-deductible expense.

The same principle applies to the plant and equipment used to run the building, from air conditioning units to lifts, lighting, IT systems and even the carpet. These don’t last forever either, in fact they last a lot less than 40 years, so they can generally be depreciated over 4-20 years. As with buildings, depreciation on plant and equipment can also be treated as an annual tax-deductible expense over the item’s life, even though there’s no actual cash cost to the carpet looking a little dated over time.

What is Tax-Deferred Income?

Australian property funds distribute income as ‘distributions’, which can include taxable and tax-deferred components. Tax-deferred amounts usually come from non-cash deductions like depreciation. These amounts are not included in the investor’s income tax return for the year; instead, they reduce the cost base, deferring tax until a capital gains tax (CGT) event.2

The key point is that although the tax system allows depreciation to be treated as an expense, it is a notional expense and doesn’t impact the amount of cash that investors receive from the property year-to-year.

That said, there’s no such thing as a free lunch. Because depreciation reduces the cost base, it can increase the capital gain when you go to sell the property or your units in a fund, and therefore the CGT bill. This is why this income is called ‘tax-deferred’ rather than ‘tax-free’.

How much of the Distribution can be Tax-Deferred Income?

Up to 100% of a property fund’s distribution may be classified as tax-deferred income, depending on many factors including:

- The age of the property – if older, the buildings or the plant and equipment may already have been fully depreciated.

- How much value is in the land – land can’t be depreciated so properties with high land value, may have relatively low levels of depreciation available.

- How much debt is used – in general, using more debt will increase the amount of tax-deferred income as a percentage of the distribution to the investor, though this comes with increased risk.

Why Tax-Deferred Income Matters

Tax-deferred income should be taken into account for the following reasons:

1. Lower Tax Leakage During Your Hold Period

Property funds typically pay distributions monthly or quarterly, providing investors with regular cash flow. Tax-deferred components can enhance after-tax returns, especially for those on higher marginal tax rates or retirees seeking income stability.

2. Compounding and Reinvestment

Tax-deferred distributions can be reinvested, allowing investors to benefit from compounding until a CGT event occurs. Over time, this can significantly increase total returns.

3. Strategic Tax Planning

Deferring tax until a capital gains event can let investors access CGT discounts. Individuals and trusts may get a 50% discount if they hold the investment for at least 12 months, while complying super funds may receive a 33.33% discount. In some cases, super funds in pension phase may pay no capital gains tax.

Case Study: Quantifying the Benefit

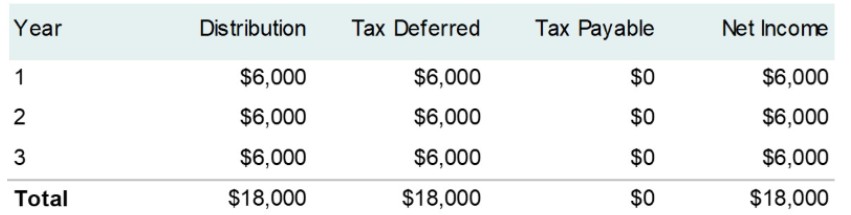

Consider an investor on a 45% marginal tax rate, investing $100,000 in a property fund paying 6% distributions, all tax-deferred, over three years.

Upon redemption, the cost base is reduced by $18,000, resulting in a capital gain. With a 50% CGT discount, the total tax on the commercial property investment is $4,050.

Were the investor to have invested in cash at 6.0% p.a. the total tax would have been $8,100 – twice the rate on the property fund.

Conclusion

Tax-deferred income offers significant advantages for long-term investors, including enhanced after-tax returns, compounding benefits, and strategic tax planning.

While the mechanics can be complex, understanding how these work can help investors make informed decisions and optimise portfolio outcomes.

For advisers, this is especially important as tax outcomes are generally specific to an individual’s circumstances. Leveraging depreciation benefits in future opportunities can improve returns and add long-term value to clients’ portfolios.

For more information, consult your tax adviser and review the latest guidance from the Australian Taxation Office.

1 This summary is of a general nature only and does not take into account the specific circumstances of an investor. This information is only current as of the date of this article. It is important that you seek professional taxation advice before you invest or deal with your investment, as the Australian taxation system is complex, and the taxation treatment of your investment will be specific to your circumstances and to the nature of your investment. It is your responsibility to consider and monitor the impact of any taxation reforms impacting your investment.

2 Please note, once the cost base is reduced to nil, a capital gain may arise to the extent of any excess tax deferred distributions (above the nil cost base).

Invest in DWAPF

Dexus Wholesale Australian Property Fund (DWAPF) is an open-ended fund that aims to provide stable returns and long-term capital growth through investment in a diverse portfolio of quality Australian office, retail and industrial properties.

More insights

Important note

Dexus Capital Funds Management (ABN 15 159 557 721, AFSL 426455) (DCFM) is the responsible entity (Responsible Entity) of the Dexus Wholesale Australian Property Fund (Fund) and the issuer of the units in the Fund. To invest in the Fund, investors will need to obtain the current Product Disclosure Statement (PDS) from DCFM. The PDS contains important information about investing in the Fund and it is important that investors read the PDS before making an investment decision about the Fund. A target market determination has been made in respect of the Fund and is available at www.dexus.com/dwapf. Neither DCFM, Dexus, nor any other company in the Dexus group guarantees the repayment of capital or the performance of any product or any particular rate of return referred to in this document. While every care has been taken in the preparation of this document, DCFM and Dexus make no representation or warranty as to the accuracy or completeness of any statement in it including without limitation, any forecasts. This document has been prepared for the purpose of providing general information, without taking account of any particular investor's objectives, financial situation or needs. Investors should consider the appropriateness of the information in this document, and seek professional advice, having regard to their objectives, financial situation and needs. This document should not be reproduced in whole or in part without the express written consent of DCFM.