Elements arrives at 80 Collins

Elements has opened at 80 Collins Street - a purpose-built wellness destination exclusive to customers within the precinct.

Welcome to "Corporate"

You are now viewing the main section of our website.

To switch to Leasing or Investing, use the menu above.

There is something unusual going on in markets right now. Traditionally, share markets and the gold price have operated inversely. When stocks are highly priced, gold tends to be unpopular and vice versa. One is risk-on, the other risk-off.

That’s not the case right now. The U.S. S&P 500 is at a record high while the ASX 200 is close to it. Meanwhile, gold, at around US$4,000 per ounce, is also near record highs. It’s a confusing environment where some investors are embracing risk by supporting high stock valuations and others are shunning it by seeking the safety of gold.

Does this mean there are no easy choices for investors seeking a sustainable and growing income stream at an attractive entry point? Absolutely not.

After a tough few years, Australian Real Estate Investment Trusts (AREITs) are set to come into their own. As our recent Reporting season wrap makes clear, the window of opportunity is wide open.

I’ll admit though that some may not see it like that. In the last two years, the S&P/ASX 200 AREIT index has risen almost 24%. How, they might ask, can AREITs still offer a compelling entry point after such a rapid rise?

The answer requires some digging. Whilst it’s true that a handful of AREITs are trading at premiums to their net tangible assets (NTA), these are overwhelmingly companies that in many countries would not be classed as real estate investment trusts in the first place.

Charter Hall, Centuria Capital and Goodman Group do not make most of their earnings from rental incomes but from funds management and property developments. These are less stable and reliable than incomes from rents, which is why in many jurisdictions their inclusion in a REIT index would be impermissible. It is also why, in the Dexus AREIT Fund, we are underweight the fund manager cohort.

Currently, Charter Hall trades at a 333% premium to NTA, Centuria Capital at 351% and Goodman Group at 175%. These three companies have had a huge impact on index returns and value.

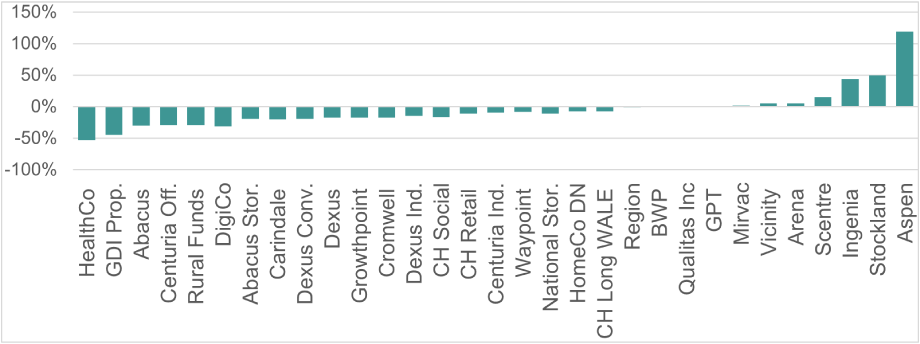

To make this crucial point clear, the chart below excludes these three companies. Had we included them, such are their massive premiums, it would be difficult to see which AREITs were still trading below NTA.

Figure 1 – Traditional rent generating REITs trades at considerable discount to NTA.

Source: Dexus

Note that most AREITs are still currently trading at a discount to NTA. Remember, too, that most derive the bulk of their income from rental streams, offering more predictable, sustainable and growing cash flows, just as one would expect from property.

It is in this area of the AREIT market, away from the fund managers and property developers, where investors can find refuge from extreme valuations and discover attractive opportunities for share-price growth.

The valuation gap presents a liquid opportunity to invest in high-quality real estate assets below their intrinsic value. The Dexus AREIT Fund is strategically positioned to capitalise on this dislocation.

The Fund is invested in AREITs with attractive, growing and sustainable yields, focusing on those that earn most of their income from rents, often with minimal running costs. These AREITs are not only undervalued but well-positioned to grow.

As inflationary pressures persist and with further interest rate cuts becoming less likely, property remains a sought-after inflation hedge.

Furthermore, with property development activity constrained, there is limited new supply. This sets the stage for rental growth and rising asset valuations. When this happens, we expect the current discounts to NTA to narrow or disappear altogether.

In the unlikely event this doesn’t eventuate, we expect increased merger and acquisition activity as larger players and private capital seek to acquire undervalued assets. This adds further upside and support for AREIT investors.

For investors seeking defensive assets with prospects for capital growth, carefully selected AREITs are an attractive candidate. An investment in the Fund offers a liquid exposure to a portfolio of AREITs with resilient income profiles, attractive valuations, moderate gearing and good growth prospects.

That’s unusual in this market. Unlike many other sectors, in commercial property the valuation cycle is in its early stages. With earnings growth forecast to accelerate, in our view, the Fund is positioned to deliver a materially higher yield and forecast to generate total returns in the low double-digits.

That’s why we consider the Dexus AREIT Fund could be ideal for investors seeking sustainable and growing income—plus the added prospect of capital appreciation.

The Dexus AREIT Fund (DXAF) is an income-focused property securities fund that invests in a portfolio of listed Australian Real Estate Investment Trusts (AREITs).

Elements has opened at 80 Collins Street - a purpose-built wellness destination exclusive to customers within the precinct.

As advisers pursue the ‘road to 200’, managed accounts stand out as a proven lever to increase productivity at scale.

33 Alfred Street has won the Heritage Development category at the Urban Taskforce Australia Development Excellence Awards 2026.

Important note: This document (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”). DXAM is a wholly owned subsidiary of Dexus (ASX: DXS). Information in this Material is current as at March 2025 (unless otherwise indicated), is for general information purposes only, does not constitute financial product advice, has been prepared without taking account of the recipient’s objectives, financial situation and needs, and does not purport to contain all information necessary for making an investment decision. Accordingly, and before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), or act on this Material, investors should obtain and consider the relevant product disclosure statement (“PDS”), DXAM financial services guide (“FSG”) and relevant target market determination (“TMD”) in full, consider the appropriateness of this Material having regard to your own objectives, financial situation and needs and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM, Level 5, 80 Collins Street (South Tower), Melbourne VIC 3000, by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1300 374 029. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives. Any forward looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward looking statements for a range of reasons. Past performance is not a reliable indicator of future performance. The forward looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments. Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material.

Connect with us to explore investment opportunities, find the right space for your best work or learn more about what we do. Together, let’s create tomorrow.