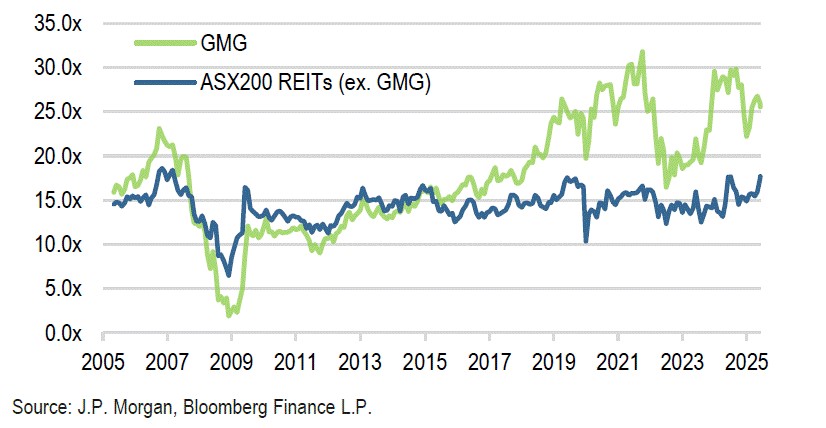

The performances of these giants skews the index. Whilst the sector remains fairly valued on earnings and asset value metrics, once the two biggest AREITs by market capitalisation are excluded, the average multiple of the remaining stocks, on a price-to-earnings ratio of around 16, looks more reasonable. The gap between the blue and green lines in the chart above makes the distinction clear.

In addition, this average multiple doesn’t incorporate the prospect of higher earnings growth. In some cases, this makes current valuations even more compelling.

So, where can conservative income inventors best find respectable yields and capital growth without undue risk?

Active management is about identifying value and balancing risk and potential reward. At Dexus AREIT Fund, we don’t invest in anything without a bullet-proof balance sheet and clear earnings growth. Here are two of the Fund's top picks that meet these stringent criteria.

Stockland Group (ASX:SGP) is Australia’s leading diversified property group with a portfolio spanning residential communities, retail town centres, logistics hubs, workplace assets and over-50s land-lease communities.

It is an under-appreciated fact that over half of the company’s net income comes from residential communities. Recent interest rate cuts and government incentives—particularly first home buyer grants—have reignited the path to home ownership.

We expect Stockland to capitalise on the rebound because it has been busy preparing for it. Australia’s persistent housing undersupply has made it a focal point for investors, provoking interest from domestic and international capital seeking sector exposure.

Two years ago, Stockland established a capital partnership to co-invest in development projects. This enables the company to fund its residential, industrial and retail development pipeline without overburdening its balance sheet. It’s a good example of Stockland’s experienced and well-respected management team planning for the future while managing risk.

With a clear growth roadmap, the company is set to deliver consistently high single-digit earnings growth over the next three years. At a valuation of 17 times earnings, Stockland offers compelling value and remains one of the Fund’s high-conviction picks.

Our next pick is Region Group (ASX:RGN), an internally-managed AREIT that owns and operates 87 grocery-anchored convenience retail shopping centres across Australia.

Retail REITs are a resilient and attractive asset class supported by steady consumer spending, high occupancy rates, and limited new supply. Along with capitalisation rate compression, these fundamentals have driven positive leasing spreads and rent growth across the sector.

Understandably, many retail AREITs have registered notable share price gains as a result. Region Group, however, despite the income stability of its underlying portfolio, has lagged. Supported by lower costs and revenue growth, we expect the company to close this performance gap.

The data is encouraging. At 3.3%, supermarket sales remain resilient while rent review increases of 4.3% among specialty tenants are boosting revenues. Region Group’s portfolio is also being carefully re-positioned to drive growth and reduce costs.

Management gets a big tick for keeping gearing in the low 30% range at a time when revaluations are rising. As for the portfolio’s cap rate, it sits at a prudent 6% while recent market transactions have occurred in the mid 5% range—highlighting further cap rate tightening.

This is a valuable reference for Region’s portfolio, reinforcing the credibility of its asset base and capital position. The recent appointment of Greg Chubb as CEO—a highly regarded figure in retail property—should deliver an even more active, performance-driven approach.

With a valuation at around 15 times earnings—well below the sector average—Region Group is set to benefit from higher net operating income, asset revaluations and new leadership.

Together with Stockland Group, it’s a perfect example of the benefits of active management in income investing.