Hot Take - What would a trade war mean for real assets?

The United States has announced a series of tariffs and other countries like China, Canada and Mexico are responding.

Welcome to "Corporate"

You are now viewing the main section of our website.

To switch to Leasing or Investing, use the menu above.

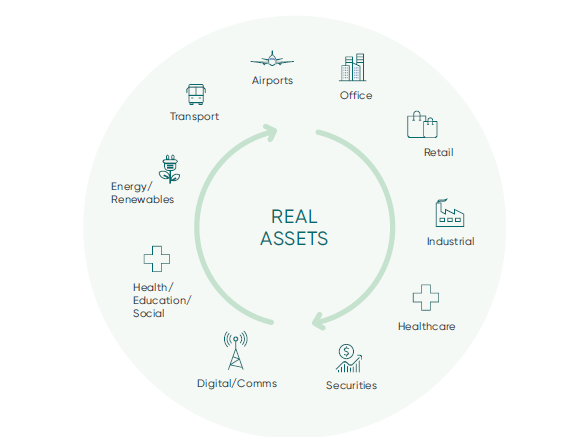

With the potential to deliver a range of portfolio benefits—from less volatile capital movements to consistent distribution streams—real assets are one of the world’s fastest-growing asset classes. As a result, demand for high-quality real assets has recently increased among professional and retail investors alike. From shopping centres, healthcare facilities, and industrial warehouses to toll roads, airports, and schools, real assets have a tangible, beneficial presence in the world.

Commercial real estate is at a pivotal moment. After years of rising interest rates and changing consumer behaviours, the landscape is shifting—bringing renewed optimism and fresh opportunities. Falling interest rates and stabilising property values are delivering greater confidence in real assets due to their ability to provide a level of tangible stability, inflation protection, and long-term growth potential. As global markets navigate economic shifts, real assets can offer a defensive investment avenue, benefiting from predictable income streams, population growth tailwinds, and sustainability-driven value appreciation.

Infrastructure and real estate both have a land component to their value, but what connects them is their importance to the economy at large and the relatively consistent distribution streams they have delivered.

Real Assets encompass everything from wind farms, life science buildings, offices, and mobile phone towers to convenience retail, airports, student accommodation, service stations, retirement living, and industrial warehouses. Diversification benefits and attractive risk-adjusted return potential make them ideal options for income-oriented investment portfolios.

In 2025, investors are increasingly drawn to real assets for their ability to hedge against market volatility while maintaining strong income generation.

Over the past 10 years, real assets—including infrastructure and real estate — have offered returns commensurate with or above those for Australian equities, at significantly lower volatility.

They are defensive thanks to the predictability of the income they deliver. Regardless of the profitability of tenants, the rent on the properties they lease—whether that be warehouses, retail space, or head office locations—is still typically reliable. This makes distributions paid from rents generally more reliable than dividends paid from corporate earnings.

Even during a once-in-100-year pandemic, assisted by the Government’s leasing code of conduct and landlord support, most rental streams held up. In a sign of their financial strength, rent collection rates have now largely returned to normal. It’s the rent collected from tenants, secured by long-term leases, that delivers the distribution of relatively high, sustainable income to real estate property investors.

The value of real assets and the income they generate tends to keep pace with inflation over extended periods.

In real estate, rents can be increased (but not reduced) over the lease period, typically triggered by inflation protection clauses in the lease or regular rent reviews. While rents can fall at the end of a lease, regular reviews may mitigate against inflation.

Many infrastructure assets also provide inflation protection through contract-mandated price increases. Both factors are particularly important to investors in retirement, who are living on the income and distributions their assets generate.

Australia is one of the few advanced countries with a rapidly growing population. As more people enter the country, real assets tend to experience more per square metre usage, without a corresponding increase in costs.

Population growth leads to highly profitable marginal income for infrastructure assets like toll roads and airports but also for real estate like shopping centres and industrial warehouses. Migration, like tourism, is great for infrastructure and real estate investors.

In the coming years, both are forecast to rise rapidly1,2, delivering a powerful tailwind to real asset investors. With urban expansion and infrastructure development accelerating, real assets are positioned for sustained demand and profitability.

From construction to everyday usage, tangible assets tend to be large emitters of carbon. Buildings are currently responsible for 39% of global energy-related carbon emissions: 28% from operational emissions, and the remaining 11% from materials and construction. That begs a question—can emissions be reduced without it costing the earth or impacting returns?

There’s a growing body of evidence indicating that investing according to ESG principles leads to higher long-term share price performance. New York University’s Stern Centre for Sustainable Business conducted a meta-study titled ESG and Financial Performance, finding ‘a positive relationship between ESG and financial performance for 58% of the corporate studies focused on operational metrics such as ROE, ROA, or stock price’.

In 2025, sustainability is no longer optional—it’s a key driver of asset value and investor preference. Real assets that integrate ESG principles are increasingly sort after, benefiting from regulatory incentives and growing demand for environmentally responsible investments.

The United States has announced a series of tariffs and other countries like China, Canada and Mexico are responding.

Our Research team shares how the outlook for commercial real estate is changing for the better, after years of rising interest rates and shifting consumer behaviours.

This material (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”), the responsible entity and issuer of the financial products of [Dexus Global REIT Fund (ARSN: 642 411 292) mentioned in this Material. DXAM is a wholly owned subsidiary of Dexus (ASX: DXS).

Information in this Material is current as at 18/10/2023 (unless otherwise indicated), is for general information purposes only, (subject to applicable law) does not constitute financial product advice, has been prepared without taking account of the recipient’s objectives, financial situation and needs, and does not purport to contain all information necessary for making an investment decision. Accordingly, and before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), or act on this Material, investors should obtain and consider the relevant product disclosure statement (“PDS”), DXAM financial services guide (“FSG”) and relevant target market determination (“TMD”) in full, consider the appropriateness of this Material having regard to your own objectives, financial situation and needs and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM, Level 5, 80 Collins Street (South Tower), Melbourne VIC 3000, by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1800 996 456. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material does not constitute an offer, invitation, solicitation or recommendation to subscribe for, purchase or sell any financial product, and does not form the basis of any contract or commitment. This Material must not be reproduced or used by any person without DXAM’s prior written consent. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives.

Any forward looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward looking statements for a range of reasons. Past performance is not an indication of future performance. The forward looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments.

Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material. By reading or viewing this Material and to the fullest extent permitted by law, the recipient releases Dexus, DXAM, their affiliates, and all of their directors, officers, employees, representatives and advisers from any and all direct, indirect and consequential losses, damages, costs, expenses and liabilities of any kind (“Losses”) arising in connection with any recipient or person acting on or relying on anything contained in or omitted from this Material or any other written or oral information, statement, estimate or opinion, whether or not the Losses arise in connection with any negligence or default of Dexus, DXAM or their affiliates, or otherwise.

Dexus, DXAM and/or their affiliates may have an interest in the financial products, and may earn fees as a result of transactions, mentioned in this Material.