Source: MSCI Australia Quarterly Private Infrastructure Fund Index

Key themes and strategic outlook

1. Energy transition acceleration

The ongoing transition to renewable energy will require large amounts of investment over an extended period. Battery storage and renewable transmission assets are attracting capital.

2. Social infrastructure and living sectors

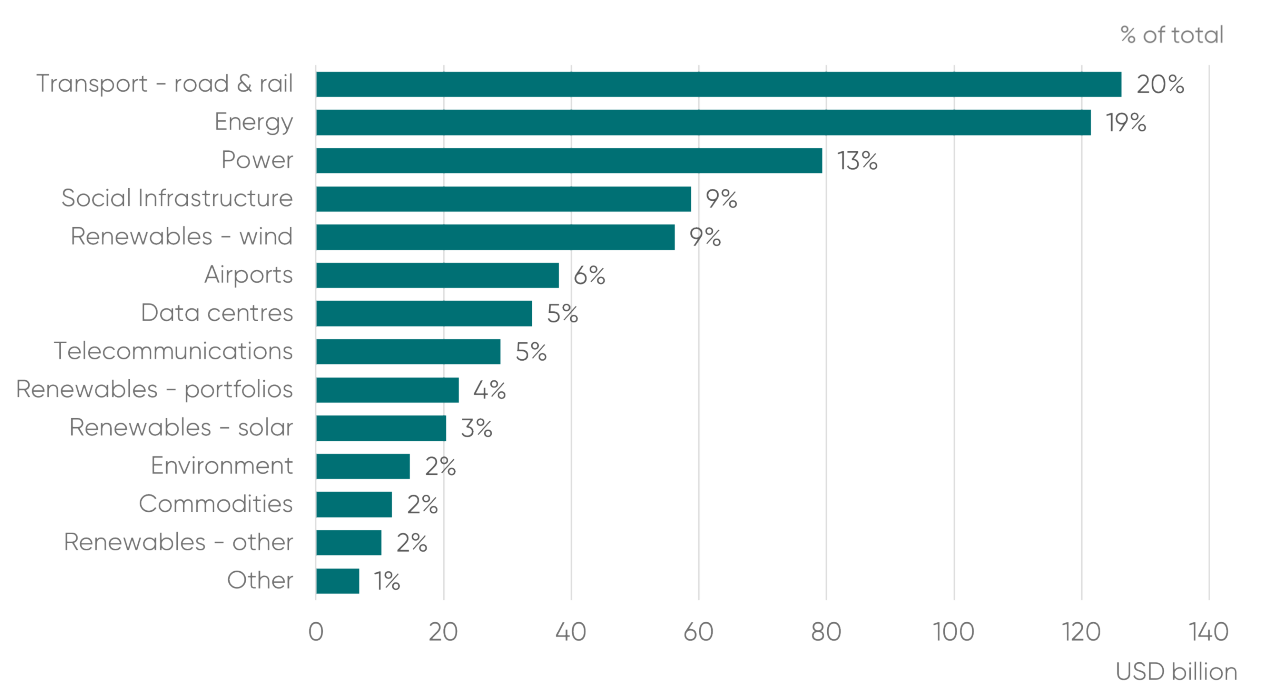

The social infrastructure and living sectors are foundational to building inclusive, and economically vibrant societies. Health services, student accommodation and affordable housing are all undersupplied in Australia, creating exciting opportunities for investment over the next decade. Over the past 5 years deal flow in social infrastructure totalled $US 59 billion comprising 9% of the total.

3. Transport connectivity and urban mobility

Metro and rail projects are reshaping urban infrastructure, with implications for land use, productivity, and asset performance. Transport projects, including airports, remain the main stay of infrastructure activity in Australia, comprising 26% of transactions over the past five years.

4. Policy, execution and income certainty

Political stability and budget clarity are enabling long-term planning and de-risking project pipelines. Infrastructure continues to offer stable, inflation-linked returns, with low correlation to traditional asset classes.

Australia’s infrastructure market in 2025 is characterised by capital resilience and thematic alignment with sustainability and connectivity goals. With robust returns, a deepening pipeline, and increasing investor appetite for energy, transport and social assets, infrastructure remains a cornerstone of institutional portfolios.

As macro conditions stabilise and execution risk declines, we believe infrastructure is well-positioned to deliver both defensive characteristics and growth optionality in the years ahead.

Read the full report here.

Unless indicated otherwise, all data referenced in this document was obtained from the following sources: