The breadth of activity was evident across a range of asset classes. We saw the acquisition of Transmission Gully by ACC for US$753 million, while in the energy and renewables sector also saw significant investment, including the purchase of Cleanpeak Energy by KKR for US$328 million and the acquisition of four renewable projects, totalling 652MW, by HMC for US$612 million. Additional activity included the sale of a 10% stake in TransGrid to GIC for US$635 million, the acquisition of Ace Power by TagEnergy for US$149 million, and the purchase of North Queensland Airports by JPMorgan IIF for US$425 million.

Powerco, New Zealand’s largest dual electricity and gas distributor and majority-owned by Dexus-managed funds, entered into an agreement to acquire Firstlight Network, an electricity distribution business serving the Tairāwhiti and Wairoa regions, owned by Clarus Group Limited – one of New Zealand’s largest energy network operators. In the same transaction, Brookfield acquired Clarus’s gas assets – Firstgas, Rockgas and Flexgas.

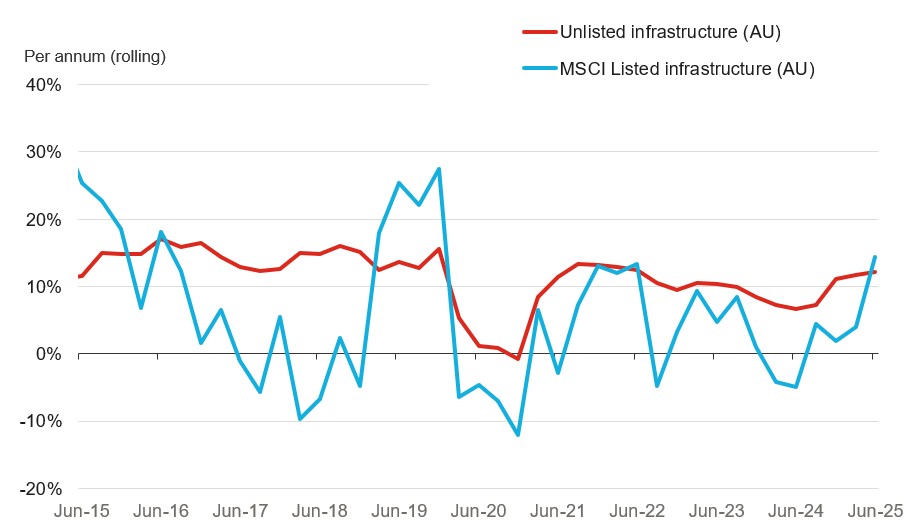

Returns and outlook

Government policy continues to underpin confidence. The Australian Federal Government remains committed to its A$60.7 billion infrastructure pipeline, with major investments targeting transport corridors, renewable energy transmission, and housing supply. In addition, the Government has set a new emissions reduction target of 62% to 70% below 2005 levels by 2035, reinforcing the focus on sustainable infrastructure.

Unlisted infrastructure delivered a significant 12.2% return in the year to June 2025, just below the 14.4% return for listed infrastructure, and we see the outlook for the first half of FY2026 for the sector as ‘cautiously optimistic’. Infrastructure originations are expected to benefit from sustained demand for real assets, particularly in energy storage, digital infrastructure and mid-market opportunities.

Australian unlisted infrastructure returns

Source: MSCI Australia Quarterly Private, Infrastructure Fund Index Australia (NAV post fees)

Australia’s economy is also showing encouraging signs. Inflation is easing, business sentiment is holding up, and we’re seeing a shift from public sector stimulus to private sector-led growth. GDP grew 1.8% over the year to Q2 2025, with forecasts pointing to 2.1% growth in 2026. Business confidence has been positive for four consecutive months, despite a softer August, the upward trend still stands. This should bode well for inbound investment in Australian infrastructure. However, the labour market is also worth watching, with jobs growth slowing to 1.5% annually.

The surge in infrastructure M&A activity across Australia and New Zealand in Q3 2025 is more than a statistical anomaly but instead is a clear signal of continued confidence and strategic repositioning within the sector. In a recent report from Infrastructure Partnerships Australia, Australia was identified as the most compelling infrastructure investment destination for the first time since 2021, surpassing North America and Europe. It also found that 85% of investors are highly likely to invest or continue to invest in Australian infrastructure.

As Australia and New Zealand move into the second half of FY2026, the sector’s outlook remains anchored by fundamentals: disciplined capital allocation, a supportive policy environment, and sustained demand for real assets. For investors, the current landscape offers both resilience and a platform for growth.

For more information: Australian Real Asset Quarterly Review Q4 2025

Unless indicated otherwise, all data referenced in this document was obtained from the following source:

Australian Real Asset Review Q4 2025.