There was a time when investing in commercial property was an “all or nothing” affair. It was impossible to purchase a part of a shopping centre, warehouse or hospital in a format that made it easy to buy and sell. Everything was purchased and sold in its entirety, which is why to this day many investors think commercial property is beyond their means.

The advent of the listed property trust sector in the 1970s made commercial property investing accessible to all. In 1971, General Property Trust became the first Australian Real Estate Investment Trust (AREIT). There are now more than 70 AREITs listed on the ASX with a combined market capitalisation exceeding $100 billion (Source: ASX).

Their success is down to a simple fact; many investors need reliable, stable yields from which to fund their day-to-day expenses. This is the AREIT sector’s reason for being, and explains why every major global sharemarket has its own REIT sector.

Beyond listed trusts like AREITs, the commercial property sector now includes property securities funds and unlisted property trusts, sometimes known as syndicates, each with their own pros and cons.

The sector is expanding in other ways, too. It is now possible to invest in childcare, healthcare, data centres and telecommunications REITs under a tax-advantaged structure that allows the buying and selling of small parcels of real estate just as you would an ordinary share, with minimal upfront capital commitment.

Why choose Australian Real Estate Investment Trusts (AREITs)?

You may not know of the term but you will almost certainly know the names. Scentre Group, Stockland and GPT Group are three well-known AREITs. Each aims to offer investors reliable, stable income by owning, managing and operating income-producing commercial real estate.

Listed on the Australian Securities Exchange (ASX), AREITs can be traded just like ordinary shares, allowing investors to purchase an interest in a diversified, professionally managed portfolio of real estate in much the same way as you might purchase shares to build a portfolio.

There are seven major benefits of using AREITs to gain exposure to the commercial property sector:

1. Easy to build a diverse portfolio

The listed AREIT sector includes thousands of properties, from shopping centres, commercial office space and healthcare facilities to self storage, data centres and warehouses. You can even access REITs in Asia, Europe and the US, making it easy to build a diverse portfolio of listed commercial property assets at home and overseas.

If you don’t want to build your own REIT portfolio, unlisted funds like the Dexus AREIT Fund and the Dexus Global REIT Fund offer a ready made solution. Actively managed funds like this charge an annual fee—under 1%—to gain access to an instant, diversified portfolio of commercial property managed by experts.

2. Simple to buy and sell

Investing in AREITs can be as easy as trading ordinary shares, and just as cost-effective. And because there’s a liquid market for most securities you can usually buy and sell when you want. Of course, you’ll need a broking account, but once you’ve got that you’re good to go.

As for unlisted AREIT funds, each produces a Product Disclosure Statement (PDS) covering how the fund works, the risks, benefits, fees and taxation implications. Once you’ve examined this document, simply complete and submit an application form available on the fund manager’s website.

3. Low entry costs

Compared to the large capital commitment required when directly purchasing a commercial property investment, buying AREITs requires only a small capital outlay - as little as the minimum parcel of securities required by your broker. In the case of unlisted funds, these often have a minimum initial investment, which can be as low as $1,000.

4. Relatively high yields

AREITs generally pay out a higher percentage of earnings as distributions than ordinary shares. They also tend to offer a more dependable, higher yield than that usually available from residential property, or from dividend-orientated shares like the major banks or Woolworths, for example. Because income is typically sourced from rents rather than more volatile corporate earnings, the sector tends to attract investors reliant on a regular income.

5. Management expertise

Each AREIT is managed by a team of specialist property and investment experts focused on maximising rental returns and long term capital growth for their investors. This also removes the need for investors to participate in rental negotiations, building maintenance and the like.

6. Tax effective

The regular income distributions from AREITs originates in the rental income received from tenants. These distributions may contain a ‘tax-deferred’ component, which occurs if a property trust’s distributable income is higher than its taxable income.

Because a trust can offset its taxable income through a range of deductions – depreciation on plant and equipment, capital allowances on building structures, interest and costs during construction or refurbishment, and the costs of raising equity to name but a few – a trust’s distributable income is frequently higher than its taxable income.

7. Capital growth

AREITs tend to be income-driven investments, which is why they attract investors seeking a stable, sustainable income stream from commercial property, with little up-front investment. Capital growth is generally consistent with inflation over the medium to long term, adding to AREITs’ defensive qualities.

What are the risks?

As with ordinary shares, AREITs can sometimes be relatively cheap and at other periods over-priced. There’s a risk that you might buy and sell at the wrong time.

Then there’s the need for diversification, across sectors and geographies. Building a sensible, high-performing portfolio of AREITs requires similar skills to building a portfolio of listed shares. You may not have the time or inclination to acquire those skills.

Finally, there’s the risk that every self-directed investor takes; whilst acquiring sophisticated analytical skills - assessing an AREIT’s debt levels, management capability and earnings capacity for example - is one thing; applying those skills successfully at a time of high emotion is another.

For these reasons, some AREIT investors prefer to pay expert professionals to develop and manage a high-performing commercial property portfolio on their behalf.

How have AREITs performed?

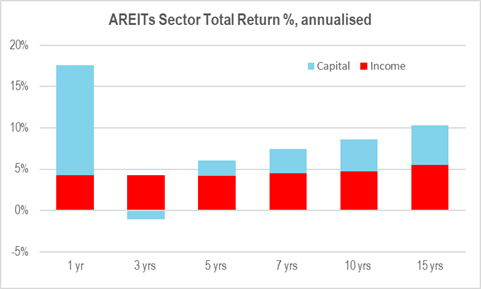

AREITs generate most of their income (circa 55-70%) from the rent collected from the tenants of the properties they own. The chart below shows total returns over the short to long-term.

Source: Dexus . As at Dec 24.

Past performance is not a reliable indicator of future performance.

The above chart shows the importance of income to total returns. Of course, the associated risk is greater than a term deposit but it’s typically lower than the kind of yield you might get from ordinary shares.

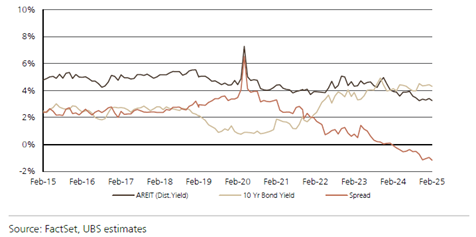

Over the last decade, AREITs have delivered an income stream, in the form of a distribution yield, consistently above the 10-year bond rate, until more recent times, where Goodman Group’s outperformance and size has had an outsized impact on the distribution yield the sector delivers. (Goodman Group’s distribution yield until recently had consistently been under 1%).

Past performance is not a reliable indicator of future performance.

What is the outlook for 2025?

In 2024, the S&P/ASX 300 AREIT index returned 17.6% outperforming the benchmark ASX 300 index by 6.2%. The pandemic, and the structural challenges it highlighted, especially in the shopping centre and office sub-sectors, meant that AREITs had been overlooked for years.

Declining interest rates have played their part. In the short term at least, as interest rates decline, the stability of the income stream an AREIT delivers tends to be valued more highly. Whether this continues is impossible to definitively say. However, by late August 2025, the Reserve Bank has cut rates three times.

There are also some sector-specific issues at play. During the pandemic, it was thought that the office market would never recover from work-from-home. In Sydney CBD for example, the vacancy rate recently peaked and planned supply is a fraction of previous levels. History has shown that office markets follow a well-defined cycle. Supply always slows after a period of high vacancy. Well located office properties offer a compelling recovery story.

After the moribund years of the pandemic shopping centres are also buzzing. Retail sales are at all-time highs, with a 10-year low in tenant occupancy costs, improved retailer profitability, near historic-low vacancy rates and positive re-leasing spreads. As our Dexus Research team recently noted in its quarterly Real Asset Review, discretionary and non-discretionary spending are rising. This is another sector set to surprise.

Finally, global uncertainty is causing coordinated downgrades to GDP growth, increasing the possibility of further rate cuts. REITs are uniquely positioned to benefit. With attractive sector valuations, we expect to see these factors play a more significant role in the months and years ahead.

Invest in AREITs

The Dexus AREIT Fund (DXAF) is an income-focused property securities fund that invests in a portfolio of listed Australian Real Estate Investment Trusts (AREITs).

Never miss an update

If you enjoyed reading this article, subscribe to the Beyond Capital newsletter and receive updates and insights straight to your inbox.

Important note

Jump to next sectionThis document (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”), the responsible entity and issuer of the financial products of the Dexus AREIT Fund (ARSN 134 361 229) mentioned in this Material. DXAM is a wholly owned subsidiary of Dexus (ASX: DXS). Information in this Material is current as at 31 December 2024 (unless otherwise indicated), is for general information purposes only, does not constitute financial product advice, has been prepared without taking account of the recipient’s objectives, financial situation and needs, and does not purport to contain all information necessary for making an investment decision. Accordingly, and before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), or act on this Material, investors should obtain and consider the relevant product disclosure statement (“PDS”), DXAM financial services guide (“FSG”) and relevant target market determination (“TMD”) in full, consider the appropriateness of this Material having regard to your own objectives, financial situation and needs and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM, Level 5, 80 Collins Street (South Tower), Melbourne VIC 3000, by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1300 374 029. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives. Any forward looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward looking statements for a range of reasons. Past performance is not an indication of future performance. The forward looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments. Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material. By reading or viewing this Material and to the fullest extent permitted by law, the recipient releases Dexus, DXAM, their affiliates, and all of their directors, officers, employees, representatives and advisers from any and all direct, indirect and consequential losses, damages, costs, expenses and liabilities of any kind (“Losses”) arising in connection with any recipient or person acting on or relying on anything contained in or omitted from this Material or any other written or oral information, statement, estimate or opinion, whether or not the Losses arise in connection with any negligence or default of Dexus, DXAM or their affiliates, or otherwise. Dexus, DXAM and/or their affiliates may have an interest in the financial products, and may earn fees as a result of transactions, mentioned in this Material.

How can we help?

Connect with us to explore investment opportunities, find the right space for your best work or learn more about what we do. Together, let’s create tomorrow.