Demographics and Technology: Themes driving Global REIT opportunity

- By David Kruth

- 11 June 2025

This article is part of a two-part series, read article one here .

In Global REITs: Standing up in uncertainty , we made the case that in a world of declining consumer confidence, falling growth forecasts and political uncertainty, real estate comes into its own.

With a focus on the Dexus Global REIT Fund, we examined two of its three pillars—the Fund’s deep defensive qualities through reliable income and an opportunistic approach to enhance returns. Let’s now turn to the third and perhaps most exciting pillar—the Fund’s relentless search for growth.

For Australian REIT investors, it can be difficult to grasp the size and breadth of the North American REIT sector, where categories like single family residences and senior housing exist alongside more familiar sectors like office and storage. This is a piece of the opportunity puzzle that warrants further explanation.

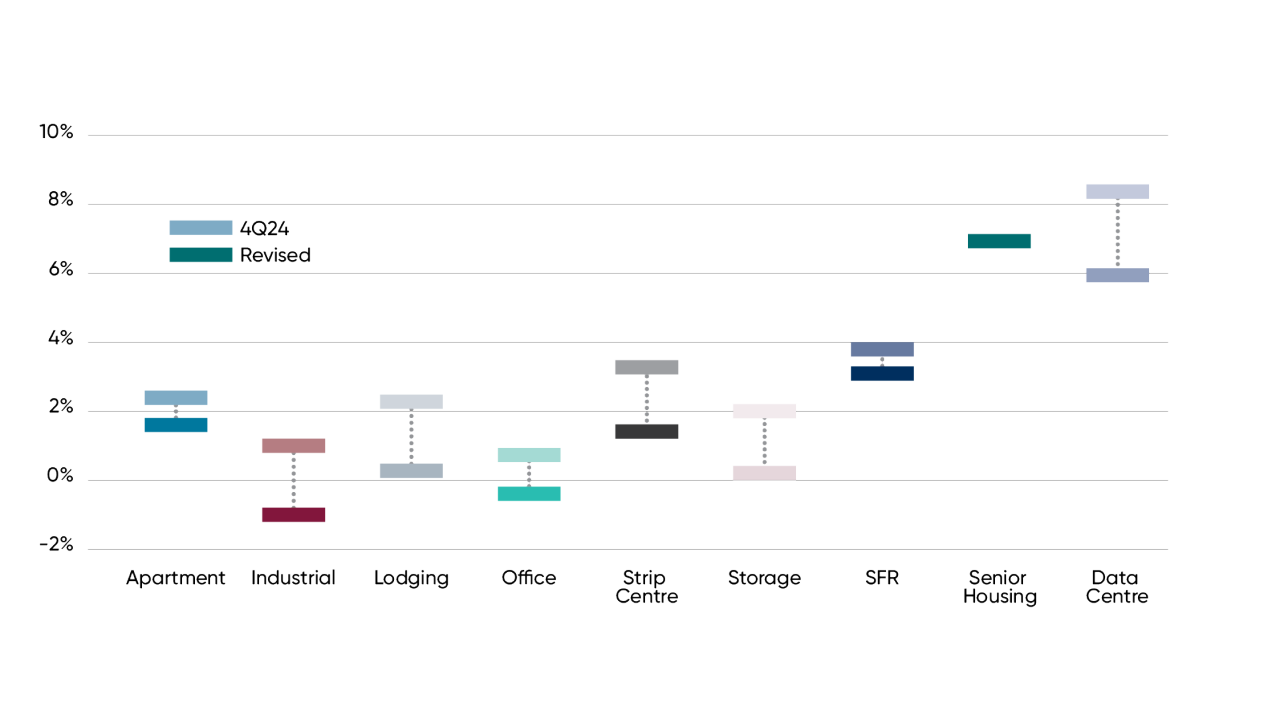

A deep and varied sector requires a metric that allows useful comparisons between REIT sub-sectors. The M-RevPAF (monthly revenue per available foot of floor area) is such a metric, popularised by Green Street Advisers.

Calculated by dividing monthly gross revenue (M-Rev) by available floor area (PAF), the space that can be leased to tenants, it measures how efficiently a REIT is generating revenue from each foot of space it owns.

When combined with compound annual growth rates (CAGR), M-RevPAF is even more useful, as the chart below shows.

Source: Green Street, Market Insight, April 2025

This is where we believe investors with an international focus can secure a relatively attractive and growing return in the years ahead.

Over the next five years, we anticipate data centres and seniors housing will enjoy 6-7% annual growth. That compares favourably to the overall real estate market growth of around 3-4%.

So, why are data centres and senior housing pockets of opportunity? Let’s deal with each in turn.

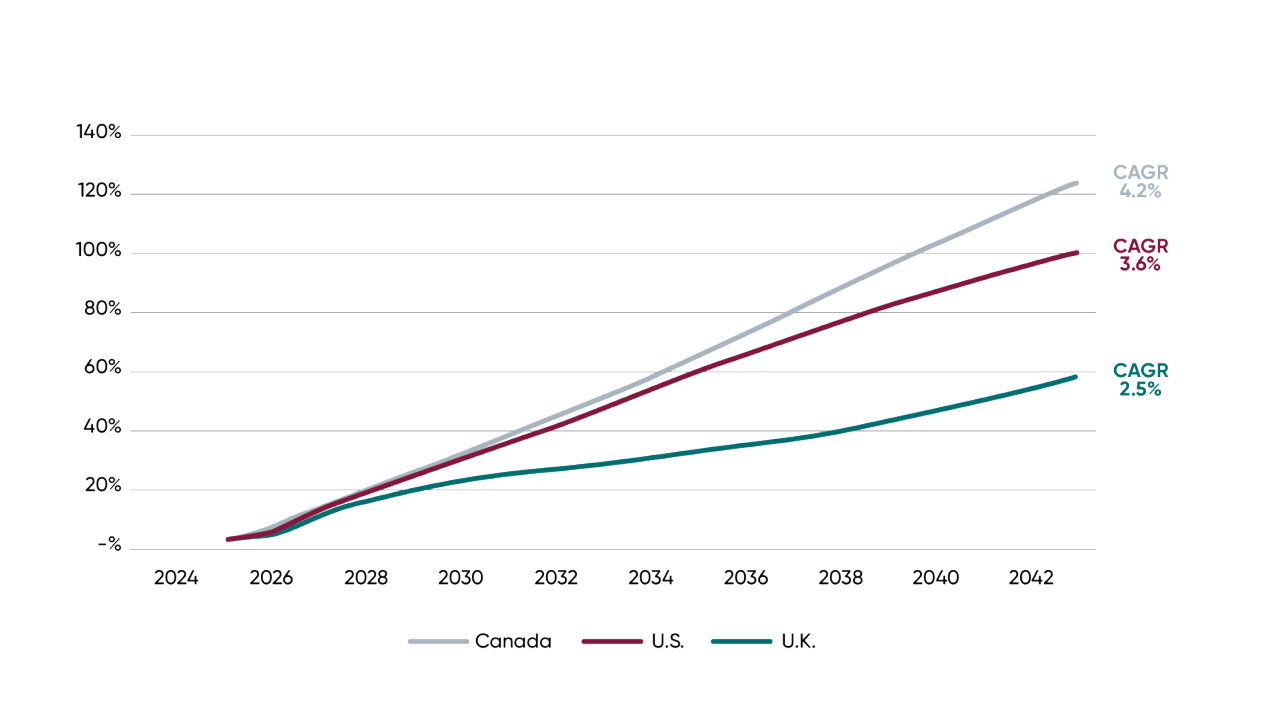

By the turn of the decade, most baby boomers (born between 1946 and 1964) will be over 70. This generation is living longer than any that preceded them. Many are expected to live well into their ‘80s and ‘90s.

Projected Cumulative Growth in Population Age 80+

Source: Cushman & Wakefield, Industry Update, Seniors Housing Outlook, March 2025

As they age, boomers want to maintain their health but also enjoy their independence and a sense of community. The traditional ‘old peoples’ home’ fails on each measure.

Developers are responding with modern retirement villages and up-market lifestyle-focused communities. As the wealthiest generation in history, many boomers have the means to pay for them. Senior housing enjoys a huge demographic tailwind.

Supply, however, is not keeping up. TD Cowan’s report on the Canadian senior housing market1 , for example, says that new starts in 2023/24 were less than 1% of existing supply and are not expected to increase this calendar year.

Meanwhile, expected obsolescence—buildings no longer fit for purpose—is running at 1-2% annually while national occupancy should surpass pre-pandemic levels this year. Despite occupancy rising above 90%, ‘CW estimates that existing rents would need to increase ~25% before more widespread development takes hold.’

These conditions are repeated across the North American market, a fact evident in the performance of Welltower, the third largest U.S. REIT.

Over the past seven years, the entire REIT sector has produced cumulative total returns of 53%2 . Welltower has delivered almost five times that figure, largely due to ~70% of its real estate value held in senior housing.

With U.S. population growth of 4% and senior housing occupancy expected to grow from the current 89% to 95% by 2029, over the next five years in our view Welltower’s net operating income may well grow at a CAGR of 10%.

This is an example of the kind of defensive real estate returns simply unavailable in Australia. Senior housing is set for long term, above-average rental growth, which is why it is a core part of the Dexus Global RREIT Fund portfolio.

To the second high-growth REIT sector.

Data Centre REITs own and operate facilities that house servers and networking equipment for cloud computing, web hosting, streaming, AI workloads and enterprise IT infrastructure.

Operating at the intersection of real estate and digital infrastructure, they’ve become increasingly attractive to long-term investors. In fact, the Dexus Global REIT Fund has direct exposure to data centres in North America, Europe and Asia.

There are similarities with senior housing. Whilst demand is growing rapidly, supply is constrained, although more so by power than access to capital.

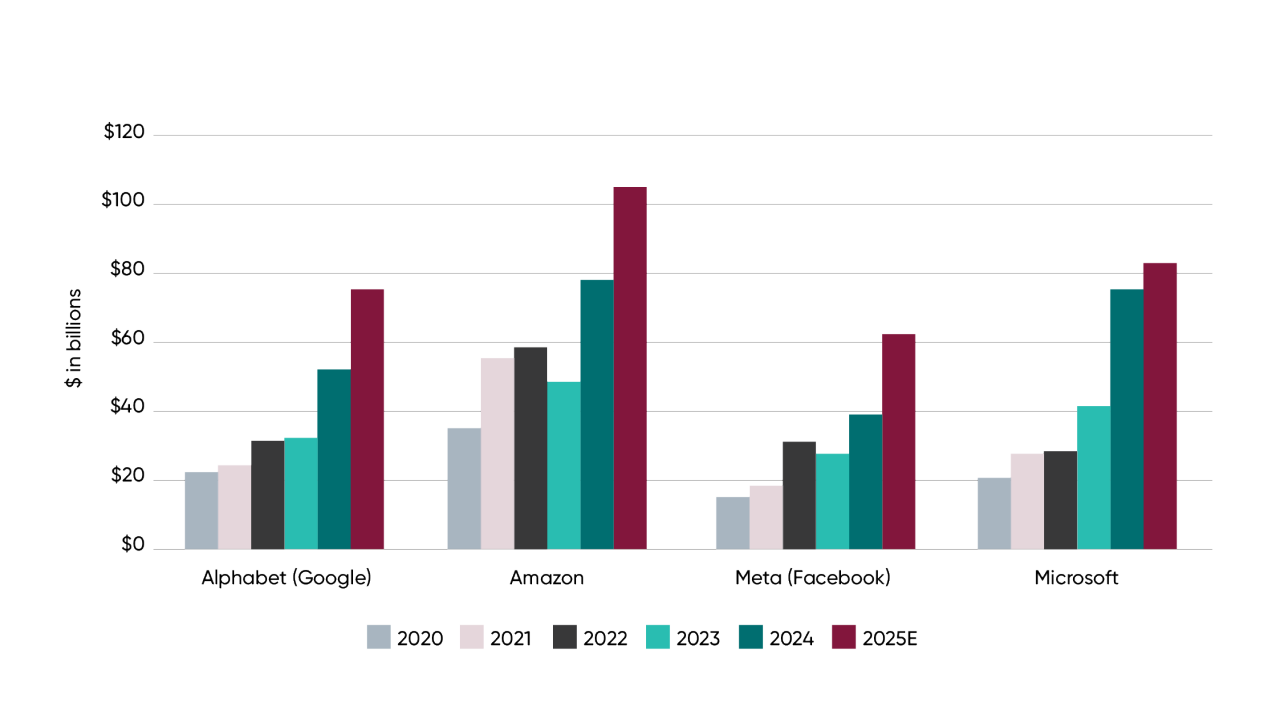

There are three kinds of data centres: network-dense, colocation, and hyperscale. Most data centres fall into the latter two categories. Hyperscalers like Google, Facebook and Microsoft are investing staggering amounts of capital to develop their artificial intelligence (AI) platforms.

This is an energy intensive activity requiring computing power on a vast scale. Or at least that was the case until Chinese start-up DeepSeek introduced AI models that consumed 50%-90% less energy during training than their hyperscaler counterparts. That prompted a severe repricing of AI-exposed investments.

Those fears now appear overdone. This year, hyperscaler tenants are expected to register record levels of capital expenditure as their cloud businesses expand and public AI adoption gathers pace.

Big Tech (Hyperscaler) Capital Expenditures

Source: Green Street, Data Center Update, March 2025

In addition to needing more data centres, these companies also need more energy to power them. Microsoft has signed an agreement to help restart the Three Mile Island nuclear plant3 , Google has partnered with a company to develop small modular reactors and Meta is also seeking nuclear generation capacity.

Again, strong demand combined with tight supply and low vacancy rates make a compelling investment case.

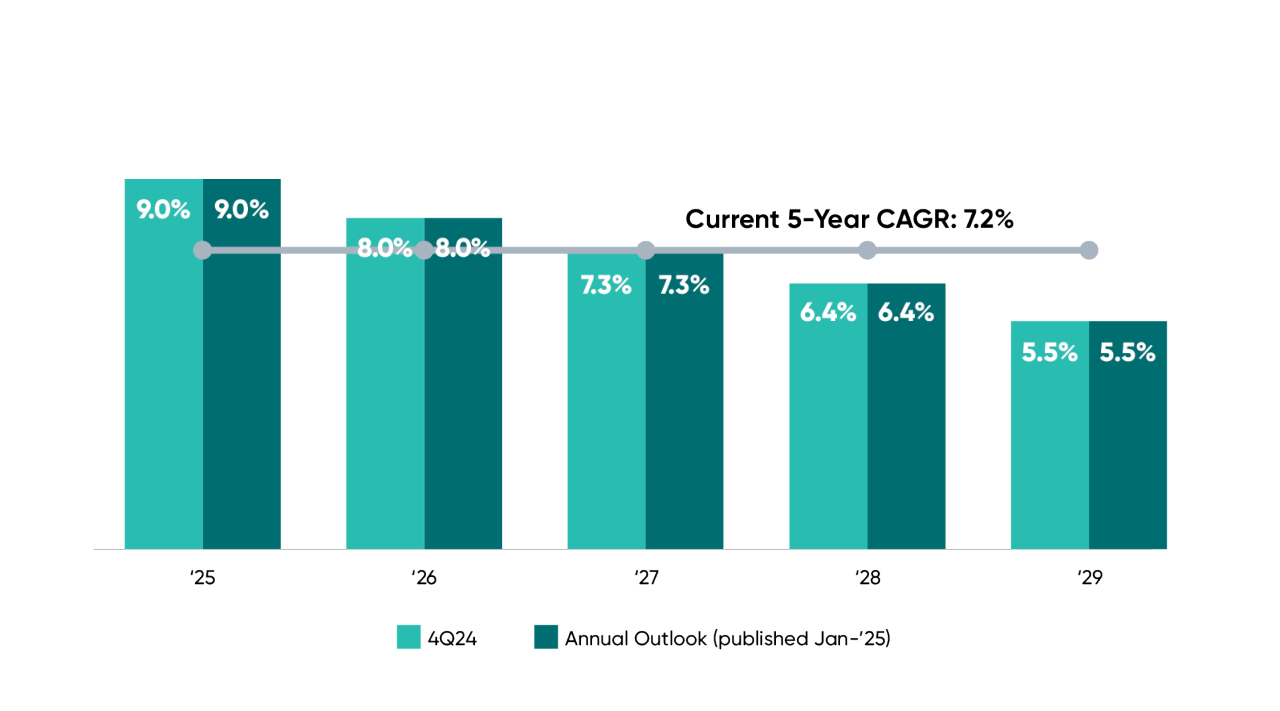

Green Street Advisers expects data centres to deliver an M-RevPAF CAGR of around 9% this year (see chart). As future data centres come on stream, Green Street Advisers expects this figure to fall to 5.5% in 2029. However, assuming that Green Street advisers is correct average returns over the period to 2029 would be 7.2%, which remains attractive.

Data Centre M-RevPAF Growth Forecasts

Source: Green Street, Data Center Update, March 2025

Satisfying that demand are established specialist REITs including Digital Realty, Equinix and Keppel Data Centre REIT. Others offering a relatively smaller direct exposure include Prologis, Segro, Goodman Group, Iron Mountain and Merlin Properties. With robust development economics and reduced risk where preleasing is possible, this is a sector offering the prospect of higher growth than other sectors beyond senior’s housing.

Future AI-infused applications will run on mobile devices, significantly increasing data requirements and demand for towers. We expect tower REITs to also enjoy a new wave of leasing requirements in 2026 and beyond.

When investing in REITs over the long term, net operating income (NOI)—rental revenue minus operating expenses—is a key driver of total returns (capital gains plus dividends). Consistent, growing NOI fuels both.

In our view, gains from higher rent and occupancy are likely to see senior housing, data centres and mobile towers deliver significantly higher NOI and earnings than every other REIT sector.

These constitute the growth pillar of the Dexus Global REIT Fund and explain why we believe it can deliver strong returns for investors in the years ahead.

Disclaimer

FOOTNOTES

1. Cushman & Wakefield, Senior Housing Outlook, March 2025

2. Green Street Health Care Insights, April 2025

3. https://www.bbc.com/news/articles/cx25v2d7zexo

Important note: This (“Material”) has been prepared by Dexus Asset Management Limited (ACN 080 674 479, AFSL No. 237500) (“DXAM”), the responsible entity and issuer of the financial products of Dexus Global REIT mentioned in this Material. DXAM is a wholly owned subsidiary of Dexus (ASX: DXS).

Information in this Material is current as at [20/12/22] (unless otherwise indicated), is for general information purposes only, does not constitute financial product advice and does not purport to contain all information necessary for making an investment decision. It is provided on the basis that the recipient will be responsible for assessing their own financial situation, investment objectives and particular needs. Before you receive any financial service from us (including deciding to acquire or to continue to hold a product in any fund mentioned in this Material), investors should read the relevant product disclosure statement (“PDS”), financial services guide (“FSG”) and target market determination (“TMD”) in full, and seek independent legal, tax and financial advice. The PDS, FSG and TMD (hard copy or electronic copy) are available from DXAM, Level 5, 80 Collins Street (South Tower), Melbourne VIC 3000, by visiting https://www.dexus.com/investor-centre, by emailing investorservices@dexus.com or by phoning 1800 996 456. The PDS contains important information about risks, costs and fees (including fees payable to DXAM for managing the fund). Any investment is subject to investment risk, including possible delays in repayment and loss of income and principal invested, and there is no guarantee on the performance of the fund or the return of any capital. This Material does not constitute an offer, invitation, solicitation or recommendation to subscribe for, purchase or sell any financial product, and does not form the basis of any contract or commitment. This Material must not be reproduced or used by any person without DXAM’s prior written consent. This Material is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives.

Any forward-looking statements, opinions and estimates (including statements of intent) in this Material are based on estimates and assumptions related to future business, economic, market, political, social and other conditions that are inherently subject to significant uncertainties, risks and contingencies, and the assumptions may change at any time without notice. Actual results may differ materially from those predicted or implied by any forward-looking statements for a range of reasons. Past performance is not an indication of future performance. The forward-looking statements only speak as at the date of this Material, and except as required by law, DXAM disclaims any duty to update them to reflect new developments.

Except as required by law, no representation, assurance, guarantee or warranty, express or implied, is made as to the fairness, authenticity, validity, suitability, reliability, accuracy, completeness or correctness of any information, statement, estimate or opinion, or as to the reasonableness of any assumption, in this Material. By reading or viewing this Material and to the fullest extent permitted by law, the recipient releases Dexus, DXAM, their affiliates, and all of their directors, officers, employees, representatives and advisers from any and all direct, indirect and consequential losses, damages, costs, expenses and liabilities of any kind (“Losses”) arising in connection with any recipient or person acting on or relying on anything contained in or omitted from this Material or any other written or oral information, statement, estimate or opinion, whether or not the Losses arise in connection with any negligence or default of Dexus, DXAM or their affiliates, or otherwise.

Dexus, DXAM and/or their affiliates may have an interest in the financial products, and may earn fees as a result of transactions, mentioned in this Material.